SynopsisThe RBI and banks are believed to be working on ways to give better public disclosure. A draft will be presented to the Supreme Court, which in 2015 mandated the RBI to disclose its supervision report if sought through RTI. While banks opposed the move, episodes of bad loans and bank troubles make for a strong pitch for increased disclosure.

Do try this at home.

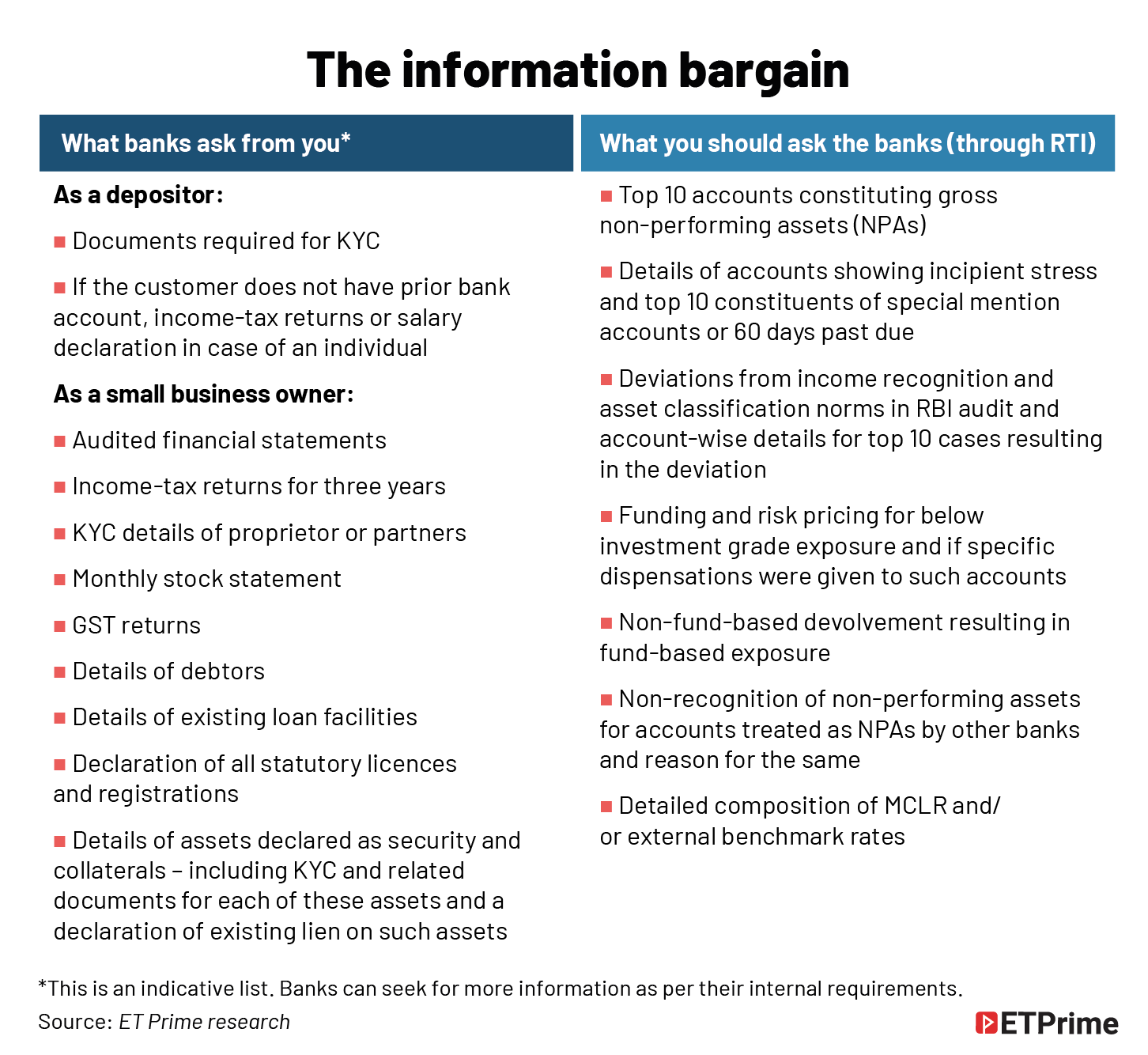

Once you make up your mind on putting your money in a bank — either in a savings or current account, or fixed deposits — make your next trip to the nearby photocopier. For, the bank will ask you to submit realms of photocopies of various personal documents to prove your domicile. In this age of extensive digitalisation, really?

And what follows? Grr. In the tiniest of fonts, the bank informs you that the data shared could be used for internal purposes that it deems fit.

But what happens once your deposit account is opened? Innumerable telemarketing calls by banks’ back offices and sales agents to sell insurance policies, loans, and credit cards. The list is long. But try asking the bank how it utilises your deposit and to whom it lends, and your query will be met with cold silence.

Now, place yourself as a small-time hotelier, who has availed an overdraft facility and a term loan from a bank. Every quarter, you would be required to furnish various details of your operations, some of which could even be confidential information. It won’t stop there. In addition to the documents required as per the loan agreement, the bank may call for more information which it believes is important. As a borrower, if questions are asked, banks are quick to respond that since they are the majority stakeholders in the business, they can ask for anything.

Both the examples cited above have a common theme. The common man barely gets to question the bank — a highly skewed practice because deposits are the bedrock of the banking business in India. They account for over half of the country’s financial savings and more than 80% of a bank’s liabilities.

Age-old twisted banking practices are set for some changes, as nearly a decade-long, fiercely fought battle for transparency has entered its last lap. Can the end result be in favour of the public at large? Before we get there, let’s first take a look at how the ball got rolling in the first place.

The game-changer fight

The judgment in the Reserve Bank of India (RBI) vs. Jayantilal N Mistry case is reckoned as a landmark in India’s financial system.

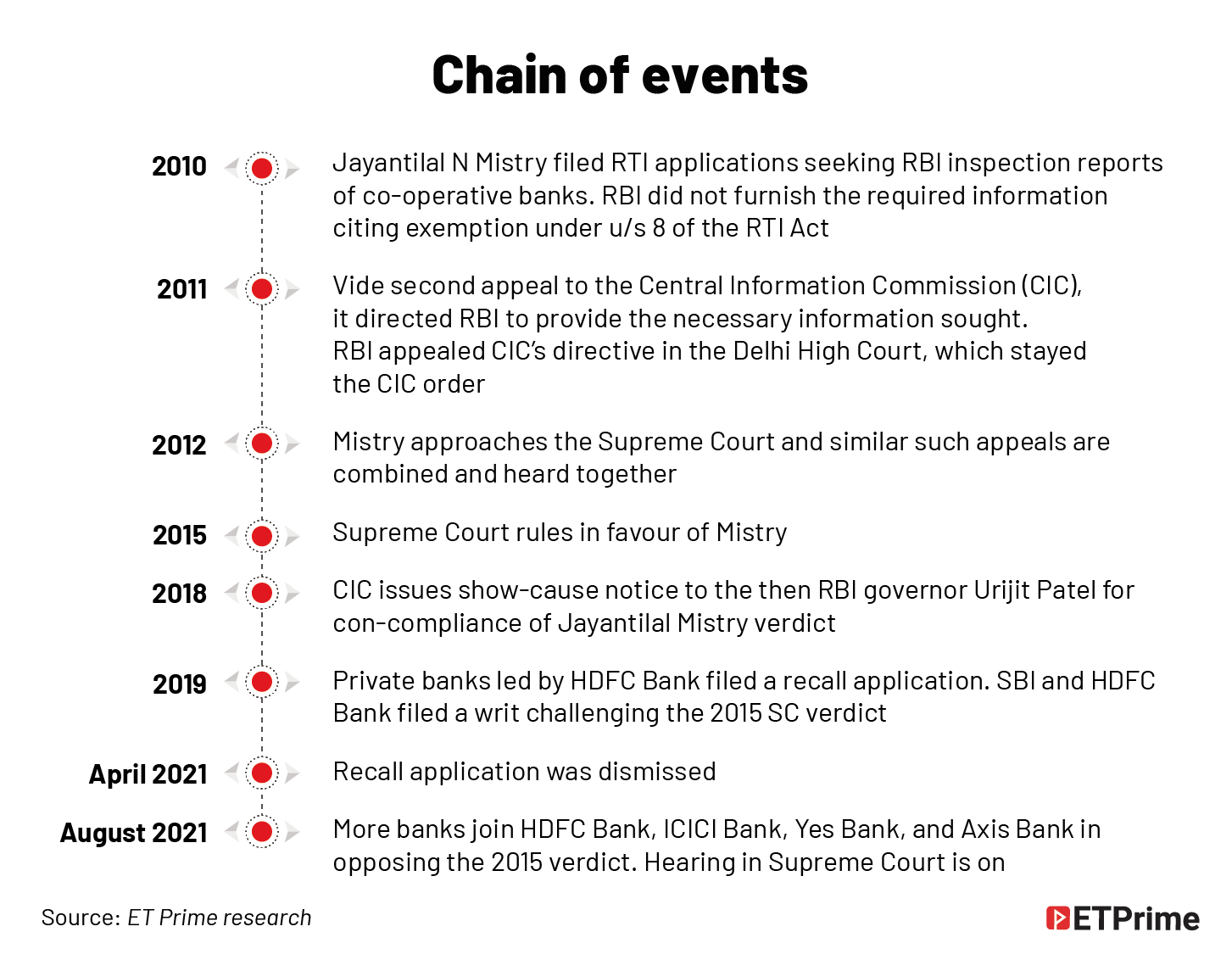

In 2010, Mistry filed RTI (right to information) applications seeking RBI inspection reports (under the Banking Regulation Act) on co-operative banks. RBI responded saying that the information sought was maintained by the bank in a fiduciary capacity and was obtained by the central bank during the course of inspection and, hence, cannot be given to outsiders. It also added that disclosure of such information may harm the interest of the bank and the banking system. Mistry did not stop short with this response.

By 2015, the case reached the division bench of the Supreme Court. The apex court’s verdict shook the banking system.

The point of contention was whether the information sought under RTI can be denied by RBI and other banks on the grounds of economic interest, commercial confidence, and fiduciary relationship. The court noted that the RBI is a statutory body set up by the RBI Act to function as India’s central bank. “Neither RBI nor banks act in the interest of each other,” the judgment spelt out. ”RBI does not obtain information from banks under the pretext of confidence or trust, and, hence, it declared that the information regarding the inspection report and other documents are liable to be provided to the public,” the verdict said.

In other words, the court held that the responsibility of RBI is to act in the interest of the public at large, and it is the central bank’s statutory duty to comply with the provisions of the RTI Act. It struck down the argument that the relationship between RBI and banks is fiduciary in nature.

The RBI did not appeal this verdict immediately. It, however, did not start complying with the order.

In November 2018, the then governor Urjit Patel received a show-cause notice from the Central Information Commission (CIC) for not honouring the 2015 judgment. In about two months, the apex court issued a contempt notice to the RBI, after which the central bank started responding to RTI applications. When certain information on the exposure of ICICI Bank and State Bank of India (SBI) to the Sahara group was sought through RTI applications, the regulator responded.

It was at this juncture that the banks got alert. They realised that disclosing information outside the template set forth in the annual report is detrimental to them. Soon, the top four private banks — HDFC Bank, Axis Bank, ICICI Bank, and Yes Bank — filed a writ petition in the Supreme Court challenging notices issued by RBI under Section 11 of the RTI Act. They also moved the apex court to recall the verdict in the Jayantilal Mistry case. In April 2021, the court turned down the recall application as not maintainable, though the writ is still being litigated.

More banks — SBI, PNB, Union Bank, Canara Bank, Kotak Mahindra Bank, and IDFC First Bank — have joined hands in the fight against additional disclosures and appealed in unison to quash the 2015 verdict.

However, for a start, RBI has asked credit-rating agencies to disclose bank-wise term-loan details of clients or the borrowers for whom ratings were reaffirmed or freshly given. ET Prime has earlier reported that corporate India has expressed its displeasure over the same.

Banks put their foot down, but what about depositors?

Among various pleas put forth by banks, including calling for a larger bench to hear the matter as against a two-member bench’s verdict in 2015, there are two arguments made by top advocates, including Mukul Rohatgi and Harish Salve on behalf of the banks, that should irk the depositors the most.

According to a Moneylife report, HDFC Bank argued that “the RBI’s inspection reports contain information about the biggest borrowers and several provisions under the RTI Act prohibit the disclosure of third-party information”. Its counsel, Rohatgi, also pointed out that when the Supreme Court has upheld privacy as a fundamental right, the loan-account details and the quantum of transactions of individuals cannot be disclosed. “Suppose Tata, Birla Group want to borrow money to develop electric cars, this commercially sensitive information is a part of the inspection reports.”

SBI’s worry is about ‘breaking the customers’ trust’. “How can we break customers’ trust by disclosing their personal info,” the bank’s counsel argued while contending that the information sought is confidential under law, and hence there is a statutory embargo on it.

The CEO of a private bank takes it a step forward. His concern is that if information sensitive to the bank is disclosed under RTI, it can have implications for the bank’s deposit base. “My fear is a potential run on the bank and subsequently, it will affect the bank’s capital position. Why should a bank, for the sake of disclosure, jeopardise its position?” he asks.

Point taken, but what about the depositors?

Among all emerging economies, India’s dependence on deposits is higher compared to China, Hong Kong, or Singapore. Yet, depositors barely have avenues to protect their interests.

In case a bank goes bankrupt, one can only hope for INR5 lakh (earlier INR1 lakh) as insurance cover from the Deposit Insurance and Credit Guarantee Corporation and that also long after the money is forgotten. What about the (paltry) interest which deposits are normally expected to earn? That, too, should be forgotten.

In simple words, the deposits are important to the banking system, but banks barely strive to protect depositors’ interest and privacy as much as they do for large corporations.

Three major troubles — Yes Bank, Lakshmi Vilas Bank, and PMC Bank, all from the private sector — in a span of 13 months from 2019 to 2020, make for another compelling reason for better disclosures. In all these cases, a certain dispensation had to be extended to ensure that the bank’s failure did not have cascading impact on the financial system of the country. Moreover, recently the government agreed to foot the bill for depositors of 21 failed co-operative banks, including PMC Bank.

While there are more private banks coming in, the asset quality of the system remains a suspect. Under such circumstances, why should the government take the burden of the private sector just to assuage the concerns of depositors?

Instead, why not enable the depositors to make an informed decision? As a former finance secretary spells out, “It’s about time to end the practice of turning to the government in case of bank failure. FDs should be on a par with any investment option.”

“Caveat emptor. Let the buyer beware” – goes the oldest, most famous, and often-used Latin legal maxim. Forming the base of any contract or commercial transaction, this principle primarily puts the onus on the buyer to be fully aware of what (s)he is shelling out money for. In any tangible transaction like purchase of a car, house property, or jewellery, the maxim is often followed. Even in financial products, like an insurance policy or mutual funds, an investor can get a handle on the end-use of his investments to a reasonable extent. Mutual funds, in particular, stand out for their transparency, with fund-related fact sheets that give the unitholder an opportunity to make an informed call and assess if the investment fits the desired risk profile.

But what option does a depositor have?

Information in annual reports or quarterly stock-exchange filings are often quantitative details. They contain details on loan growth, products that contributed to the growth, bird’s eye view of asset quality, and the overall capital position. But it’s often the qualitative aspect with respect to loans and advances that results in a bank going bad. Yes Bank, Lakshmi Vilas Bank, and PMC Bank were cases of indiscriminate lending practices that led to capital erosion. While 2015’s asset-quality review and RBI’s move to push certain companies towards insolvency proceedings in the subsequently years was a good barometer to judge how many banks were under the water, a voluntary mechanism to seek loan details could go a long way in preventing another mega bad-loan mess in India. After all, it’s well-established that transparency leads to better governance.

“RBI does not obtain information from banks under the pretext of confidence or trust, and, hence, the information regarding the inspection report and other documents are liable to be provided to the public.”

— A Supreme Court judgment in 2015Poor disclosures, a global problem

In the US, people are protesting against the confidential supervisory information (CSI) report published by the Federal Reserve. Peter Conti-Brown, associate professor of financial regulation at The Wharton School of the University of Pennsylvania, made a compulsive pitch for overhauling the practices. “The problem with the existing state of the art of the CSI is that the countervailing goal — public accountability for banks and bank supervisors — is almost completely missing,” he notes. Brown presents three ways to remedy the situation:

- Completely abolish CSI, as a concept forged in the mid-20th century may not have the resilience to work in the 21st century.

- Disclose specific aspects of the examination process from examination reports, call reports, and the final rating assigned by the supervisor to each of the bank.

- Just like the monetary-policy deliberations, preserve and disclose everything even though it may be after a lag.

The debate about the CSI was set to roll in 2019. Though finality is still miles away, sources privy to the development say Congress is well aware of the demand to revise the extant law and the matter is expected to be taken up soon.

How to avoid a rubber-stamp process

Indians aren’t alone in this fight for transparency.

Unlike the West, India has a powerful information-seeking tool — the RTI Act. But the possible flip side is that sensitive information may be shared with just a few, and public interest may not be served in totality. Also, as Rohit Raghavan, partner at law firm Saraf and Partners, puts it, the concern is whether the present format of supervision report yields itself to easy comprehension.

“Given the complexities involved in the [RBI’s inspection] report, its format is not one which is suitable for public disclosure, because it’s not prepared to make it public,” he says. “It will have to be a delicate balance between all the parties involved – the court, RBI, and the banks.”

Highly placed sources indicate that RBI is deliberating on a format for disclosure if the Supreme Court upholds the 2015 verdict.

However, it may end up as a namesake public-disclosure format if the regulator and the banks get into a huddle to decide what information should be revealed and what should be kept away.

Can the court step in to ensure that the proposed format doesn’t become a rubber-stamp process? Well, that’s a million-dollar question.

Banking is a dynamic business, and that should be acknowledged while formulating the format. In a particular year, if there’s a specific point that needs to be revealed to the depositors, the format should have the room to accommodate such one-offs. Banks divulging watch-list details or troublesome loan accounts to investors in 2016 is an example.

Further, like in RTI applications where past information can be sought, the format should also have similar flexibility. This is particularly important to trace if loans are sold down or taken over by banks.

So, coming out with a template for disclosure has its own limitations.

The third likely option is the chief risk officer and the chief executive officer (CRO and CEO) of the bank giving a declaration that there is no departure in NPA-recognition norms followed by the bank, and that it is exactly according to the IRAC (income recognition, asset classification) requirement laid down by the RBI. Such a declaration on a monthly or quarterly basis would help the depositor assess the risk position of the bank.

But whatever option the court decides, one thing is certain. We are nearing the last leg of ensuring better transparency in the banking system. “The case right now is a call for more transparency in the system and the end result of this litigation will result in better disclosure,” Raghavan believes.

We believe that, too.

(Graphics by Mohammad Arshad)

The latest from ET Prime is now on Telegram. To subscribe to our Telegram newsletter click here.