If OPD coverage is built into a policy, or is offered as a rider, the limit will be specified

OPD expenses, while individually small, can sometimes become reasonably large over the entire year, especially in families where there are children and senior citizens

OPD expenses, while individually small, can sometimes become reasonably large over the entire year, especially in families where there are children and senior citizens

Since the onset of the pandemic, demand is up – not just for comprehensive health insurance covers but also for outpatient department (OPD) covers.

Reliance General Insurance has recently launched Reliance-Digital Care Management, a policy that covers OPD expenses with sum insurance ranging between Rs 1,000 and Rs 5,000.

OPD policies are available in three formats.

“It sometimes comes as a built-in benefit within a comprehensive health policy. It is also available as a rider,” says Indraneel Chatterjee, co-founder, RenewBuy. Standalone policies with sum insured up to Rs 1 lakh are also available.

Tackle recurring expenses

The majority of health insurance plans do not offer OPD benefits.

“The bulk of out-of-pocket expenses on health care, however, arise due to OPD expenses,” says S Prakash, managing director, Star Health and Allied Insurance.

Adds Amit Chhabra, head-health insurance, PolicyBazaar: “Almost everyone, irrespective of age, incurs OPD expenses.” These plans usually cover costs like doctor’s consultation fee, annual health check-up, pharmacy bills, diagnostic tests, and dental and ophthalmic treatment. Some also cover costs incurred on physiotherapy, vaccination, AYUSH treatment, etc.

A standalone OPD cover will have its own sum insured. If OPD coverage is built into a policy, or is offered as a rider, the limit will be specified.

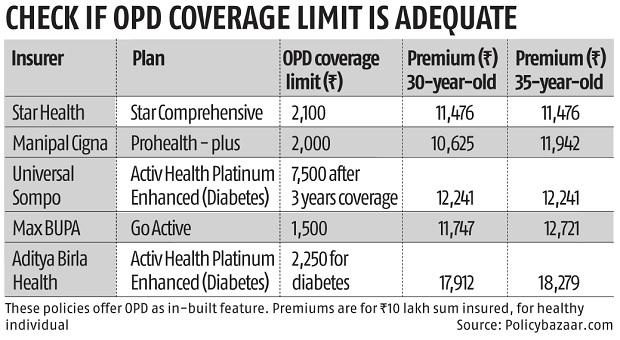

Watch out for limits

Check whether the sum insured for OPD coverage is adequate.

“Estimate your household’s annual OPD expenditure and then decide on the sum insured you should buy,” says Nayan Goswami, head-general insurance, Sana Insurance Brokers.

Prakash says that in this age of investigative medicine, when costs incurred on diagnostic tests can be high, one should have OPD coverage of Rs 50,000-1 lakh for the family.

Next, check the sub-limits.

“If the total OPD coverage is for, say, Rs 10,000 in a year, there could be sub-limits for consultancy, diagnostics, and medicines. Make sure these are adequate,” says Jitendra Singh, vice-president, Swastika Insurance Broking.

Sometimes there is a sub-limit on each consultation. “If your plan pays only Rs 350 or Rs 500 for each consultation, that may suffice in a small town, but not in a metro,” says Goswami.

Some plans impose restrictions on consultations with specialists, like two in a year. “Such low limits could be inadequate for families that have children and senior citizens,” says Goswami.

If you have a pre-existing disease, you are likely to face a waiting period. Go with a plan where it is low. Check whether the OPD facility is available within a closed or open network of hospitals and doctors.

Both options have their pros and cons.

“When an insurer offers this facility only at network hospitals, it is able to maintain tighter control over costs and is able to offer more attractive pricing,” says Chhabra. However, this can at times be inconvenient.

“It means your options will get restricted to the insurer’s panel of doctors,” says Singh. The cashless facility is usually available only at network hospitals. Some insurers even impose co-payment if you consult outside the network.

What you should do

Purchase a comprehensive health insurance plan first. Remember that although hospitalisation is rare, the cost incurred on each incident is high.

“Buy a high-quality base policy that offers good OPD coverage as a built-in feature. Several recently launched plans offer this,” says Chhabra.

If your base cover does not offer OPD as a built-in feature, but the company offers a good rider, go for it. If not (or if you want a large sum insured), buy a standalone cover.

Prakash suggests going with an insurer with a reputation for offering quality service, including easy cashless claims, on OPD expenses. These policies are usually issued on the basis of self-declaration, so be truthful. Finally, you can avail of Section 80D deduction on a standalone cover too.

Points to remember when buying an OPD policy

- The sum insured should be adequate for your family’s requirement

- The limit on payout for each consultation should not be too low

- The limit on number of consultations with specialists should also not be very low

- Watch out for co-payment requirement, especially for consultation at a non-network hospital