SynopsisThe Insolvency and Bankruptcy Board of India or IBBI, the insolvency regulatory body set up as per the Insolvency and Bankruptcy Code, turns five this October. It has received both criticisms and plaudits. Be it regarding resolution timelines or recoveries in DHFL and Jet Airways. But the key question remains: has it been able to deliver the desired results?

On October 1, 2016, one of the biggest reforms in the economic history of India began. Under the Insolvency and Bankruptcy Code or IBC, the Insolvency and Bankruptcy Board of India or IBBI — the regulatory body meant for strengthening the identification and resolution of insolvencies in a time-bound manner — was established.

Until then, failed businesses and the stakeholders involved were at the mercy of litigations, multiple windows and the course of time for justice and closure.

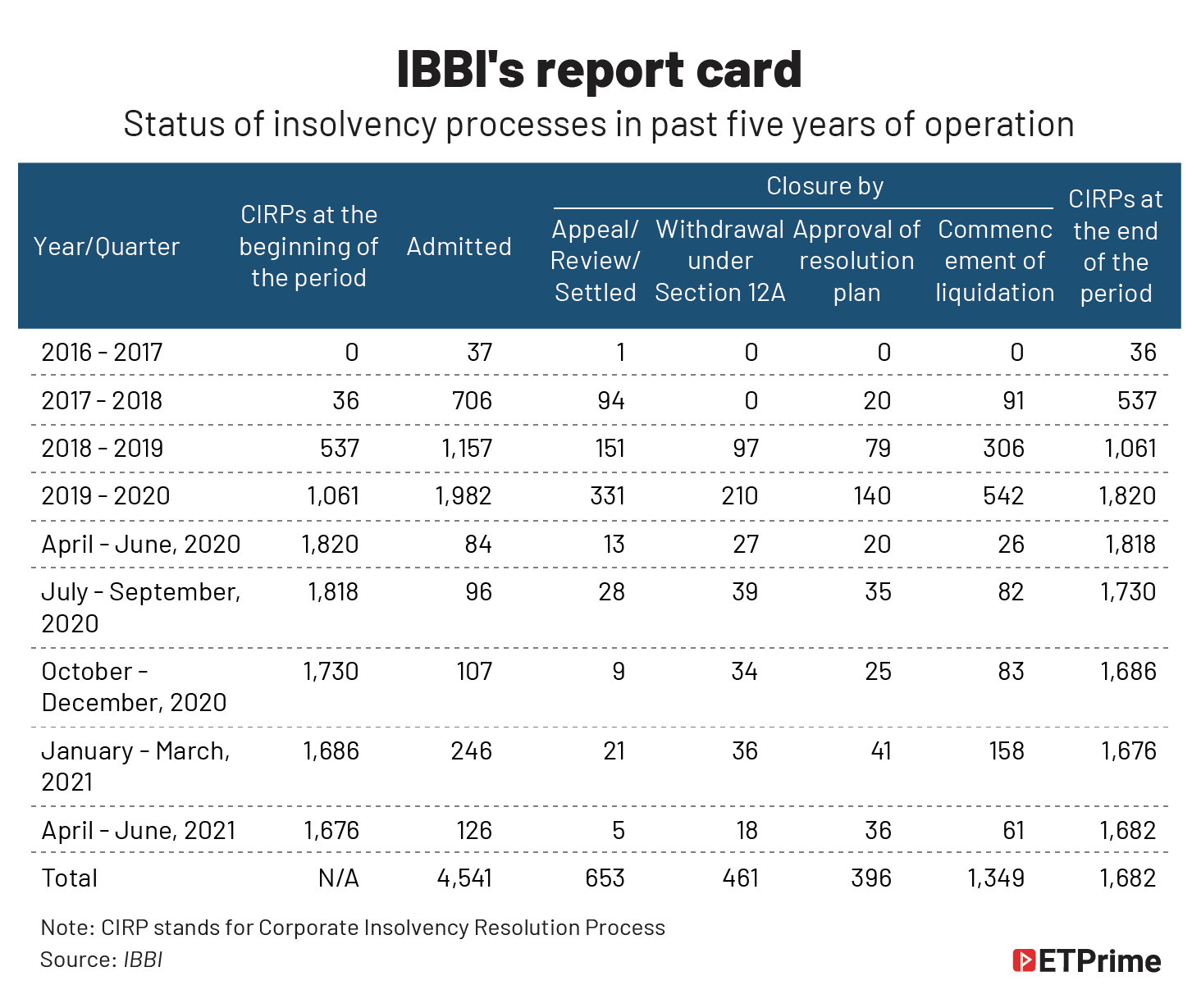

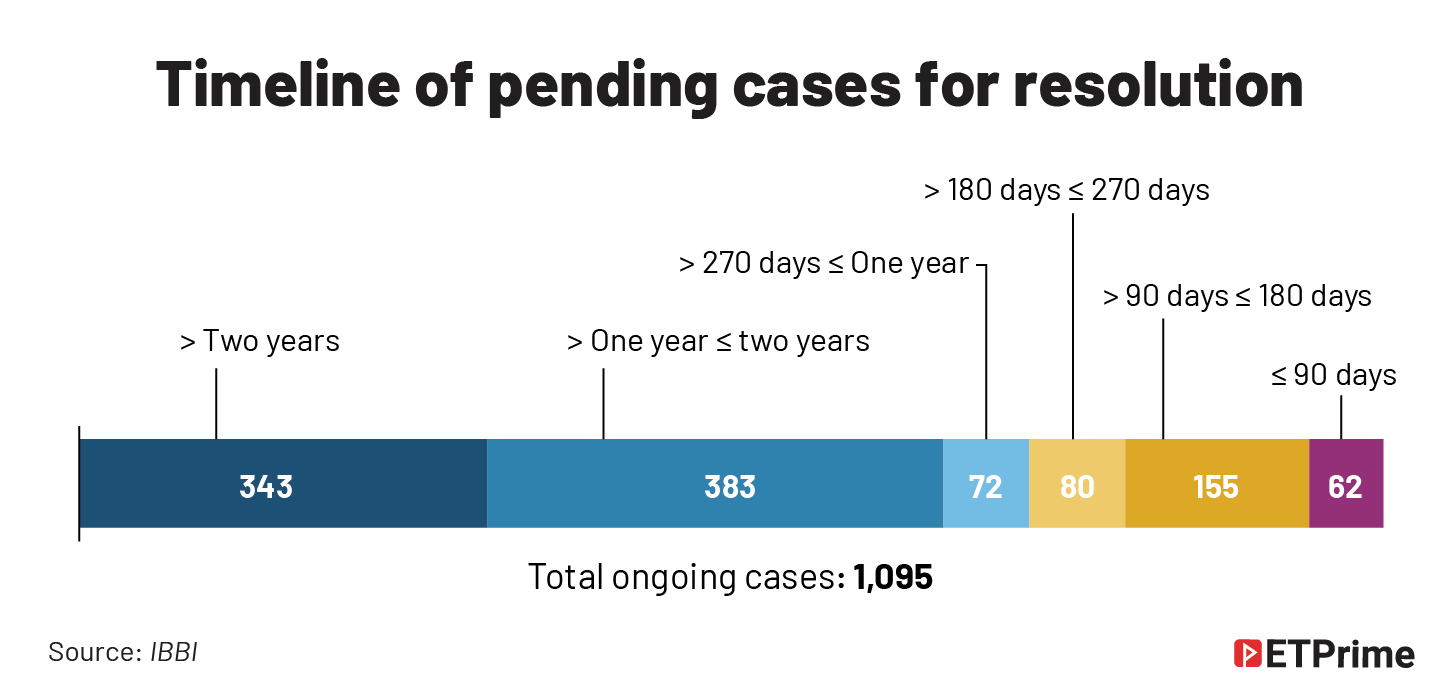

This year, IBBI completes five years of its operations but the going hasn’t been easy. For perspective, currently over 1,000 cases are pending under IBC of which 343 cases have been ongoing for the past two years. The pandemic, with its unnatural business environment, amplified the frequency of companies approaching the IBBI for resolutions.

But, in the past five years, has it been as effective as it was thought to be? In fact, it has attracted the attention from both sets of people. Some call it a game-changing legislation, while others have criticised it for failing to deliver timely resolutions and leading to massive haircuts during the recovery of bad debt.

IBBI’s journey as the regulatory body for the implementation of IBC so far has not been an easy ride.

The beginning

There have been attempts at insolvency reforms in the past, such as debt-recovery tribunals, Lok Adalats, and the Securitisation and Reconstruction of Financial Assets and Enforcement of Securities Interest Act (SARFAESI). But they have had limited impact.

The ever-mounting problem of non-performing assets (NPAs) triggered the need for comprehensive legislation for insolvency and bankruptcy. The foundation of IBC was then laid down with the formation of the Bankruptcy Law Reforms Committee (BLRC) in August 2014 headed by TK Viswanathan (former Union law secretary and secretary general Lok Sabha).

“When the code and the IBBI were brought to life, there was no capacity or experience of insolvency resolution, as envisaged under the code. Established in October 2016, the IBBI was instructed to commence corporate insolvency by December 1, 2016.”

— MS Sahoo, chairperson, IBBIThe draft of the Insolvency and Bankruptcy Code 2015, based on the BLRC report, was then introduced in the Lok Sabha in December 2015 by former Finance Minister Arun Jaitley. The code was referred to a joint committee of parliament and was later passed in the monsoon session of the parliament in June 2016.

Criticisms and plaudits

One of the most vocal critics of the performance of IBC and its custodian IBBI has been the Standing Committee of Finance chaired by Jayant Sinha. Interestingly, Sinha was the minister of state (finance) when the legislation saw the light of the day.

The committee’s report on the IBC pointed out various shortcomings. The report stated that the IBC has low recovery rates and the creditors are taking haircuts as high as 95%. It further highlighted that over 71% of the cases are pending for over 180 days, which goes against the objective of the code of providing timely resolutions.

According to the report, out of 20,963 cases pending admission in tribunals, 13,170 cases are of IBC, with an amount involving INR9.20 lakh crore.

The committee has also recommended having a benchmark for the quantum of haircuts which is comparable to global standards.

Does that mean the IBC and IBBI have been a complete failure?

Experts that ET Prime spoke with believe there have been quite a few misses, but the legislation is still work in progress and there is a long road ahead.

“There is no doubt that with the advent of the code, more particularly, the ‘creditor-in-possession’ model, we have lately seen that borrowers now tend to observe credit discipline,” said Diwakar Maheshwari, dispute resolution partner, Khaitan & Co, a Mumbai-based law firm.

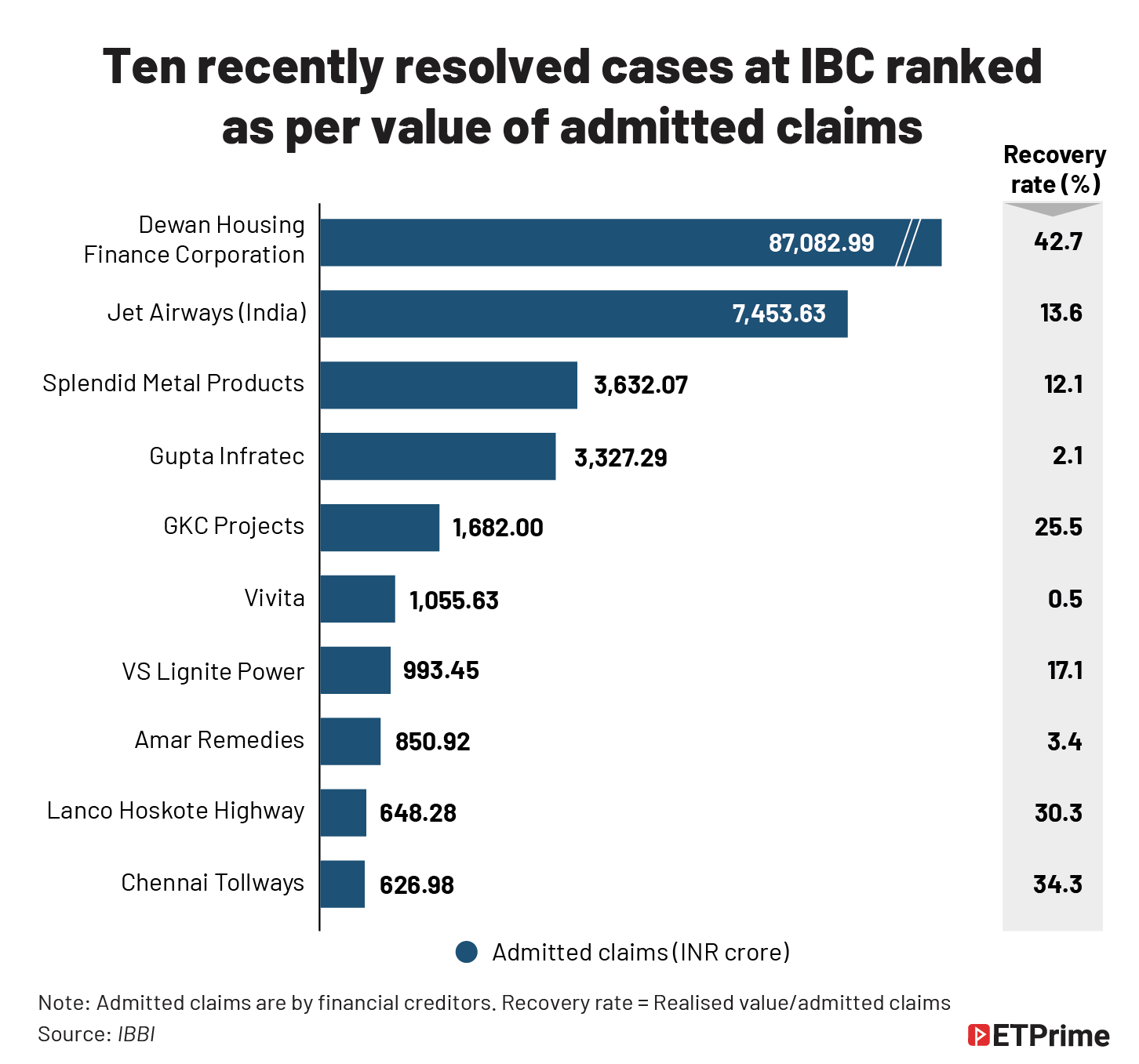

The recovery rate is measured as the percentage of the amount recovered by creditors from the total amount due. However, these assets are distressed, and in many cases the corporate debtor was either under Board for Industrial and Financial Reconstruction (BIFR) or defunct which makes the overall recovery rate skewed.

“The realisation value by creditors should be compared with the liquidation value, which is a better metric to evaluate the performance of IBC. This metric is much higher, over 1.5x,” said Suharsh Sinha, partner (insolvency, bankruptcy and restructuring), AZB & Partners, a Mumbai-based law firm.

“Also, we need to take into consideration that the recovery rate is determined by the market forces as envisioned in the code,” he added.

As of June 30 2021, realisation value of financial creditors in comparison to liquidation value is 167.95%, on the other hand the realisation value in comparison to their claims is 36%, according to IBBI data.

The bug in the business

The IBC does provide a timeframe within which the resolution process should conclude.

However, once the resolution plan is approved by the creditors committee it further needs a nod from the National Company Law Tribunal or NCLT.

And that is where most of the delays happen.

“NCLT needs more infrastructural support. It is short-staffed and the lack of institutional capacity has delayed the insolvency process in many cases. Also, it desperately needs a framework regarding entertaining frivolous appeals filed by the former promoters of the corporate debtors,” Sinha adds.

The Standing Committee also took cognisance of the fact.

The panel called out the Ministry of Corporate Affairs for failing to fill in vacancies at these tribunals. The report highlighted that there were only 29 NCLT members against the sanctioned strength of 63. Also, most benches of the NCLT only sit for twice a week as members divide their time between other benches. This has led to significant delays in resolution.

Learning by experience

IBBI, the sole custodian of the code, has been closely monitoring the progress of the IBC and has been taking steps to plug loopholes and perceived defects. The board faced multiple initial glitches to put together the framework in place.

“IBBI didn’t even have a proper office to start with. It started operating from a small office set up at the ICSI office in Delhi. The board was also short of human resources while forming the regulatory framework for one of the biggest financial reforms of the country. We used to start our day early and used to put in extra hours most of the days,” one of the industry experts involved in the initial process told ET Prime.

“When the code and the IBBI were brought to life, there was no capacity or experience of insolvency resolution, as envisaged under the code. Established in October 2016, the IBBI was instructed to commence corporate insolvency by December 1, 2016. The immediate tasks included: market volunteering to set up IPAs (insolvency professional agencies), individuals with the right calibre to enrol with IPAs and seek registration with the IBBI as insolvency professionals (IPs), CIRP and liquidation process to be in place, spread the message of the code and make the stakeholders aware of their role,” MS Sahoo, chairperson, IBBI told ET Prime.

“Every new case was a learning for us. It helped us in making the code even stronger as the days passed,” said the industry expert quoted above.

One of a kind

On January 23, 2017, NCLT had admitted its first case — Synergies Dooray Automotive Limited under the new bankruptcy code. In August 2017, NCLT passed its first order under the IBC allowing Synergies Dooray’s merger with its subsidiary.

This case proved to be a significant one in many ways. Not only was it the first resolved case under the new legislation but also helped in overcoming initial inhibitions.

People familiar with the early days told ET Prime there was a sense of nervousness and hesitation regarding admitting new cases and writing orders as this was supposed to set up a precedent for the future orders. Nobody wanted to go wrong. Things became a bit smooth after the first order was passed in the case of Synergies Dooray. Later, the cases also paved the way for a particularly significant amendment to the code — Section 29A.

The turning point

There have been as many as six amendments to the IBC and various other amendments to the regulations. While many amendments have been passed to make clarifications or to make minor tweaks in the procedures, a particularly significant amendment was the addition of the Section 29A.

The IBC, in its original form, had not incorporated any provisions to prevent defaulting promoters from buying back the corporate debtor. Section 29A was inserted with a retrospective effect from November 23, 2017.

It prohibited certain “undesirous” or “unscrupulous” persons from bidding for the assets of the debtor company and effectively barred the erstwhile promoters from regaining control of the company at the end of the resolution process.

The idea behind this amendment was that earlier the promoter could allow his company to default on its debts, have a portion of the debts forgiven in the resolution process, and regain control of the company.

Making homebuyers stronger

A landmark case, which led to another amendment, was of Jaypee Infratech.

Consumer creditors were not part of the stakeholders that the IBC intended to consider initially. However, in August 2017, when the case of real-estate developer Jaypee Infratech was admitted, it was observed that homebuyers who had paid advances to the developer were as aggrieved as any other creditor. If they didn’t have any say in the insolvency process, they wouldn’t get either their homes delivered or refunded.

IBC took this fact into consideration and treated homebuyer advances of an under-development project as well as financial creditors, entitled to similar recoveries.

Immunity of Section 32A

The addition of this new section insulated successful bidders from any investigations from the Enforcement Directorate or Sebi for any wrongdoings by the corporate debtor in the past before it went into insolvency.

This helped in getting high-quality bidders to participate in the process who were earlier hesitant in bidding for companies already under investigation.

Successful resolution of DHFL

“Another significant achievement of the IBC and IBBI is the successful insolvency of an NBFC — DHFL. It is first of its kind and could have been easily considered as one of the most complicated cases handled by the board,” says Vivek Parti, an insolvency professional based out of Delhi.

DHFL was the first case of a financial-services provider that had come for resolution under the IBC. Insolvency of an NBFC was not part of the initial code, however, the Reserve Bank of India and the NCLT worked in tandem and succeeded in resolving DHFL that went to Piramal Capital and Housing Finance.

Taming the committee of creditors

One of the major recommendations of the Standing Committee on Finance is to introduce a professional ‘code of conduct’ for the Committee of Creditors (CoC), which is the most important decision-making body of the IBC framework.

The committee report highlighted that CoCs now enjoy complete autonomy in taking commercial decisions.

“The code provides a creditor-in-control process for insolvency. The commercial wisdom of the CoC is supreme and not justiciable. However, there have been instances where its conduct has not been above board, at times threatening integrity of the resolution process. In consultation with the Indian Banks’ Association, the IBBI is working on the guidelines to stipulate conduct expected from a CoC,” Sahoo told ET Prime.

The way forward

The IBC and IBBI have made major strides in the past five years overcoming various institutional and infrastructural challenges. The IBC regime is much ahead of its predecessors. However, the outcome has often been far from satisfactory, be it in terms of timelines or recoveries for creditors.

Many new regulations are currently ‘works in progress’ which need to be rolled out sooner. Pre-packaged resolutions, group insolvencies, cross-border insolvencies and individual insolvencies should be prioritised by the board.

Speaking of pre-packaged resolutions, they have already been rolled out and an application related to GCCL Infrastructure and Projects has already been admitted.

“The uniqueness of this code has been that all the amendments brought since its inception have been by way of ordinances only. This clearly demonstrates the keenness and open-mindedness of the government to address the various nuances of the code as it evolves with time basis judicial guidelines, various expert committee reports and practical learnings on a real-time basis,” said Maheshwari.

According to Sahoo, “We have just scratched the surface. As we crossed a small mountain, a much bigger mountain became visible.”

(Graphics by Mohammad Arshad)

The latest from ET Prime is now on Telegram. To subscribe to our Telegram newsletter click here.