SynopsisSharp & Tannan, Chaturvedi & Shah, and KK Mankeshwar & Co were auditors of CG Power in the years between FY15 and FY19. Their role in not flagging alleged fraudulent transactions and irregularities is a matter of investigation, State Bank of India, the lead lender for CG Power, tells CBI.

Gregory (Scotland Yard detective): “Is there any other point to which you would wish to draw my attention?”

Sherlock Holmes: “To the curious incident of the dog in the night-time.”

Gregory: “The dog did nothing in the night-time.”

Holmes: “That was the curious incident.”

(The Adventure of Silver Blaze, Sir Arthur Conan Doyle)

The statutory auditors of CG Power & Industrial Solutions did nothing when alleged fraudulent transactions worth thousands of crores took place till a stormy board meeting in August 2019.

Yet, these watchdogs have had a long leash these two years when almost every other party associated – promoters, directors, executives, and even lenders – has been facing difficult questions from regulators and investigative agencies.

That leash might tighten in the coming days, with State Bank of India (SBI), the lead lender to CG Power, specifically naming the firms and partners that functioned as statutory auditors between FY15 and FY19.

SBI has named three leading audit firms and four of their partners in its complaint to the Central Bureau of Investigation (CBI). CBI has registered a case based on this complaint, which includes CG Power’s erstwhile chairman Gautam Thapar, directors, and other unknown people as accused.

SBI named Sharp & Tannan, which was associated with CG Power for a major part of the past two decades; KK Mankeshwar & Co, which had mandates across several group companies, including BILT; and Chaturvedi & Shah, which had a brief stint as a joint statutory auditor in FY17.

The complaint identified Milind Phadke (FY15 and FY16) and Vinayak M Padwal (FY17) of Sharp & Tannan; Parag D Mehta (FY17) of Chaturvedi & Shah; and Ashwin Mankeshwar of KK Mankeshwar & Co (FY18 and FY19) as the partners who signed the financial statements.

“The partners of the statutory auditors signed off on the audited balance sheets of the company and did not highlight the fraudulent transactions and the various irregularities. However, this is a subject matter of investigation,” SBI general manager Suresh Kumar Pareek said in the complaint.

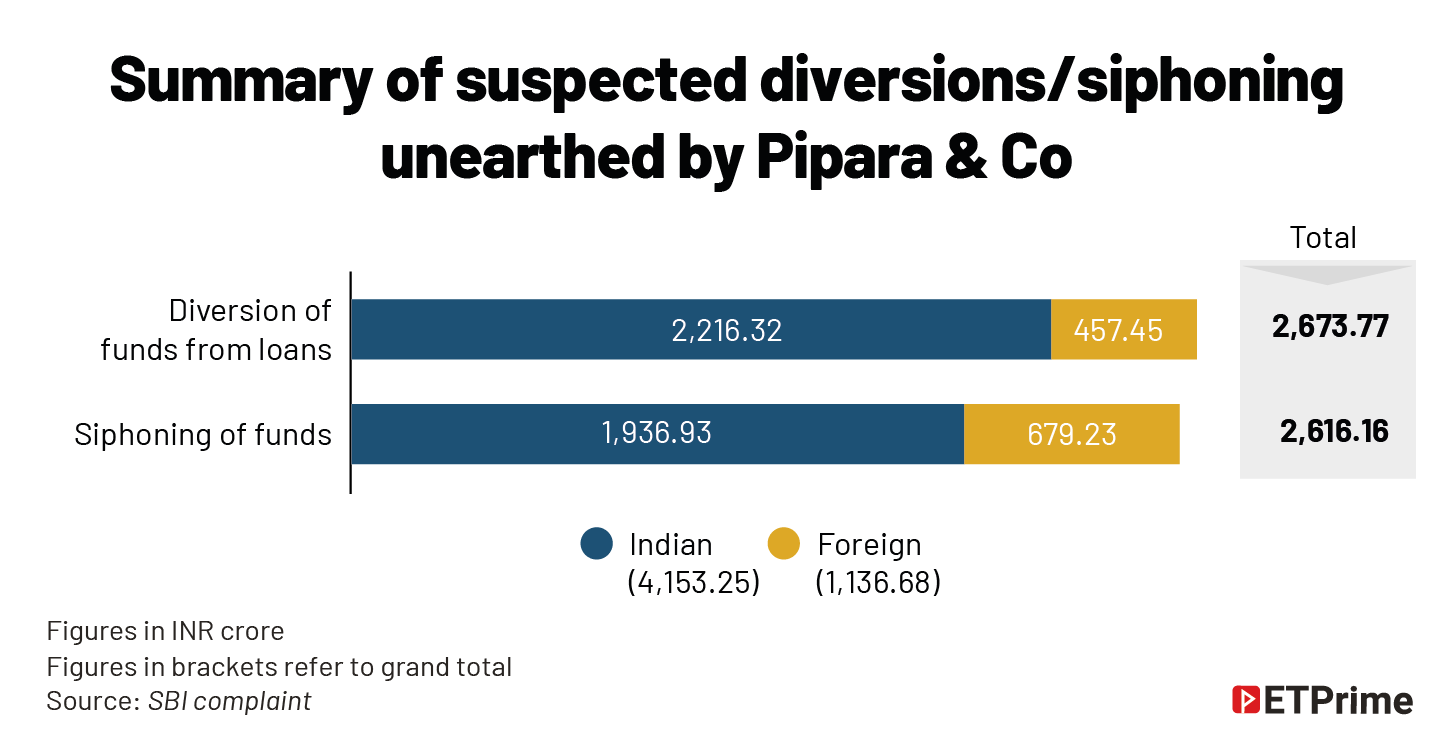

SBI had assigned Ahmedabad-based Pipara & Co as the forensic auditor. According to the forensic auditor, the fraud occurred from FY14 to FY15, and FY18 to FY19.

The forensic audit has flagged as many as 19 major transactions where instances of fund diversion or siphoning were noticed. According to Pipara & Co, the total value of these suspected transactions was over INR5,289 crore.

Of these audit partners, Phadke passed away in June 2016. Sharp & Tannan had inserted an obituary ad in Times of India in remembrance of its senior partner. Padwal, Mehta, and Mankeshwar did not respond to e-mail queries sent by ET Prime.

Long association and non-audit fees

Long association and non-audit fees are considered to be factors affecting the independence of statutory auditors. This had prompted the legislators to bring in new provisions in the Companies Act, 2013, to restrict tenures to a maximum of two consecutive terms of five years each. Rules were also introduced to mandate the rotation of auditors.

However, these did not immediately end existing relationships.

In a report in February 2020, Bengaluru-based proxy advisory firm InGovern Research Services, raised several questions on the role of auditors in CG Power and the red flags they ignored. It also highlighted Sharp & Tannan’s long association with CG Power.

InGovern said in its report, “Sharp & Tannan have been the statutory auditors of CG Power for a major part of the last two decades, over 20 years, having been associated from even before FY1997 till FY2017 when their then-tenure ended, and they decided not to seek re-appointment. Many of the transactions occurred during the tenure of Sharp & Tannan.” An e-mail sent to Sharp & Tannan group managing partner Shreedhar Kunte did not elicit any response.

In FY16 Chaturvedi & Shah was appointed as joint statutory auditor but had to step down during FY19. After this, the company hired SRBC & Co (an EY network firm) and KK Mankeshwar & Co as its joint statutory auditors in its annual general meeting of 2018.

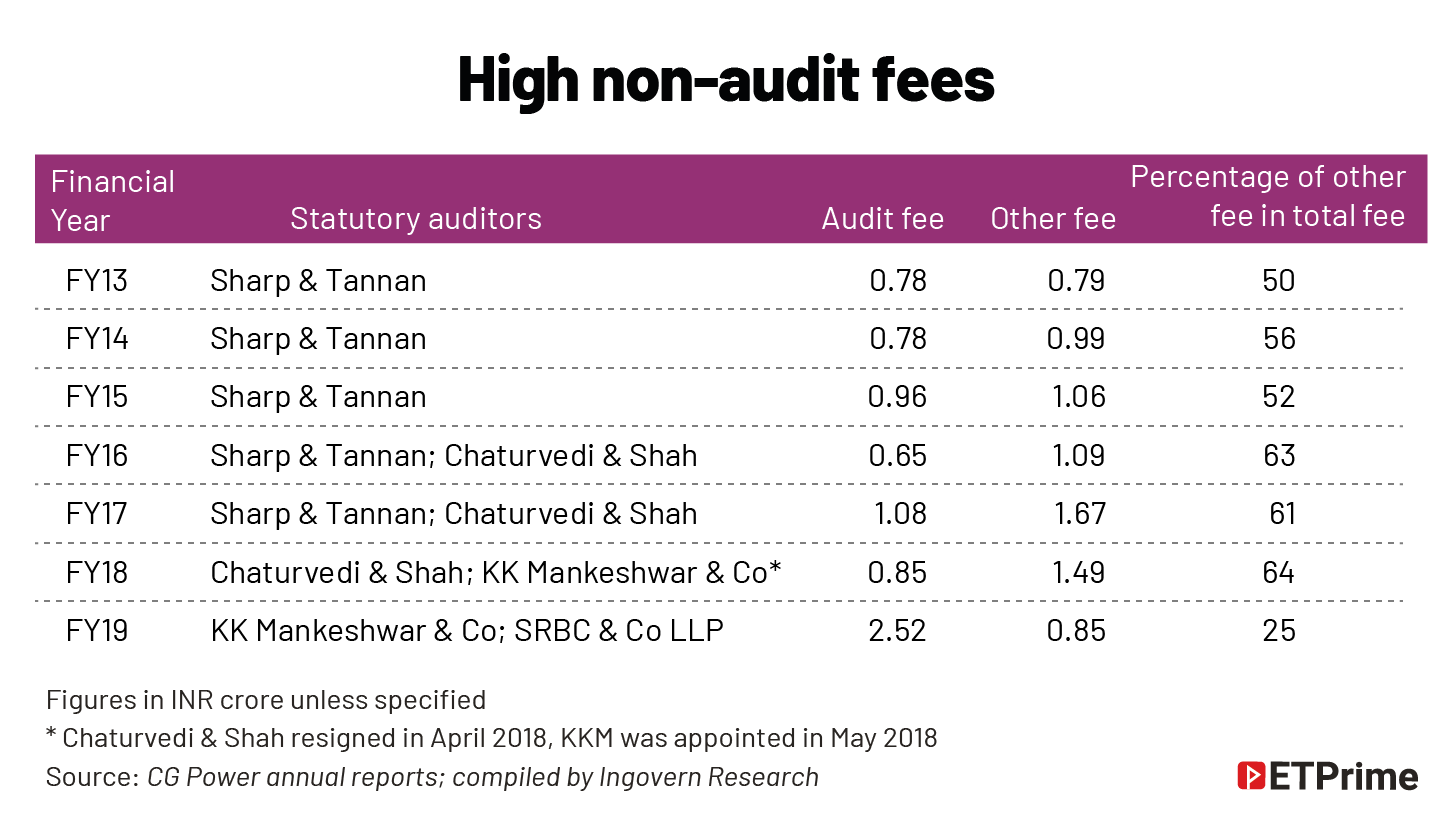

“A look at the annual reports of the previous years (excluding FY19) shows that the fees for non-audit services (which includes tax-audit fees, certification work, fees for other services, and expenses) have usually been more than 50% of the total auditors’ remuneration for any given year,” the report said.

According to InGovern, as a good corporate-governance practice, it should be ensured that non-audit fees never exceed 30% of the total auditors’ remuneration. “Arrangements such as these should be treated as red flags and concern should be raised by shareholders to their Boards,” it added.

With Phadke’s passing, the focus is now on Vinayak Manohar Padwal, who was the signing partner for Sharp & Tannan in FY17.

Padwal has over 27 years of experience in auditing and advising a broad range of local and multinational (listed and unlisted) companies in the public and private sectors. Over the years, he has had stints with top audit firms such as Kalyaniwalla & Mistry, KPMG, and BDO.

According to his LinkedIn profile, Padwal’s stint with Sharp & Tannan started only in June 2016, the month of Phadke’s demise and ended in March 2018, when he joined BDO.

A month after the CG Power revelations, in September 2019, The Economic Times reported that Padwal was joining Mazars, a global accounting network based in France.

However, his current LinkedIn profile does not indicate any association with Mazars. He is described as an “independent finance professional” and an independent director in two companies, namely Fomento Resorts and Epiroc Mining India.

While Padwal did not respond to queries, his quote in a 2018 article by The Economic Times following an order by the Securities and Exchange Board of India (Sebi) against PricewaterhouseCoopers, where the regulator punished the firm, is relevant. “Appointment of an auditor is made in the name of the firm, not the partners. If the governance system of the firm has failed, one cannot quarantine just the partners and not punish the firm,” Padwal, then managing partner at Sharp & Tannan was quoted in the article.

There is a mention of Padwal in the forensic audit report of MSA Probe Consulting ordered by Sebi. Unlike the audit by Pipara & Co, which has mentioned five financial years from FY15 to FY19 as the period of fraud, the MSA report took up only two financial years under the head, “role of statutory auditors”, which were relevant to the transactions referred to it. These were FY17 and FY18. Of these, Sharp & Tannan and Chaturvedi & Shah were joint auditors in FY17.

Against the names of Sharp & Tannan and Padwal, the MSA report said, “As the relevant transactions were not audited by them, there is no further discussion on their role.”

Experts feel that though it is common to define the scope of work in advance in case of joint audits, there are discussions about each other’s findings and exchange of notes before the balance sheet is signed and “true and fair view” is certified. Therefore, Sharp & Tannan cannot be completely absolved, they feel. Further, Padwal himself was a part of the Risk and Audit Committee that was privy to the loans given by CG Power to Avantha Group firms.

Against Chaturvedi & Shah and its partner Parag D Mehta, the MSA report said, “Audit of corporate accounts of CG Power was part of scope of work.”

‘Questionable responses and afterthought’

Parag D Mehta’s profile on Chaturvedi & Shah’s website says he qualified as chartered accountant in 2003 and became partner in 2008.

“Extensive experience in the field of statutory audit and tax audit of corporate leaders in industry namely petrochemicals and petroleum, textile industries, airline industries, telecom sector, advertising agency, media and entertainment, etc. He focuses on exploring opportunities and leveraging them to enhance the growth and expansion of the firm,” the profile reads.

According to the division of scope of work between the joint auditors, the corporate accounts of the company under which the loans are given and taken and also the sale of core assets of the company, should have been undertaken by Chaturvedi & Shah.

Mehta, in his submission to MSA also confirmed that Chaturvedi & Shah “had audited the loans and advances given and taken at the corporate level by the company during FY16-17”.

Based on this, MSA had posed certain queries on the accounting aspects of the movement of proceeds of the loan from Aditya Birla Finance routed through the Blue Garden structure. An advance of INR143 crore that was received by CG Power from Blue Garden was adjusted against loan to Avantha Holdings Limited (AHL), vide an entry dated March 31, 2017.

As AHL was holding approximately 34% shares in CG Power and had a substantial closing balance of INR102 crore outstanding, the ledger of transactions with AHL should have been scrutinised in detail.

Further, as a related party, the summary of all the transactions is disclosed as part of the financial statements. During the verification of the figures reported against the same disclosure, the adjustments of INR143 crore should have been analysed in detail.

When asked about this, Chaturvedi & Shah said, “The ledger for AHL provided to us during the course of our audit did not reflect any entry of INR143 crore being adjusted against the balance of Blue Garden. No such entry was reflected in the ledger provided to us by Blue Garden either.”

The forensic auditors found these responses unconvincing.

“The statutory auditors are claiming that they have been provided a ledger copy of AHL in the books of CG Power that was different from the one that we have received from the company. We find it difficult to believe, as the auditors are provided direct access to the computerised accounting data of the company. In such a case, how did they receive a different ledger is questionable.”

Further, MSA observed that the “auditors have not provided us with any ledger copy that was provided to them. In such a case, the statement made by the auditors is questionable.”

The year-end balance of AHL and Blue Garden in the books of CG Power would have differed by INR143 crore had the mentioned entries been omitted from the ledger provided to the auditor. However, the year-end balance as reported in the financial statements and that of the ledger of AHL reflect the same balance — INR102.70 crore.

“In our opinion, the claim of having been provided with a different ledger is an afterthought by the auditors, only pursuant to the query raised by us,” the forensic auditor concluded.

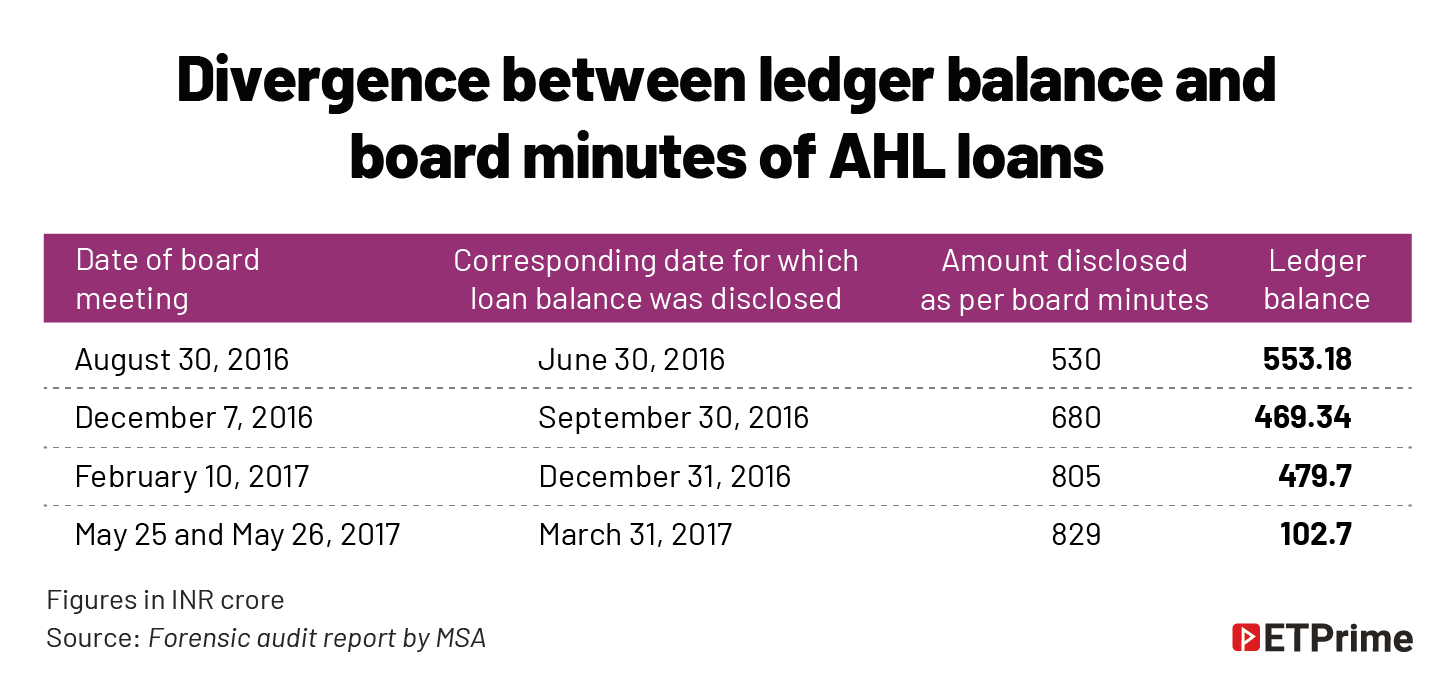

Further, there was also a substantial difference in the amount of loans given to AHL between the ledger balance and what was disclosed in the board minutes. At one point in May 2017, the difference was as high as INR726 crore.

When the forensic auditor asked about this, Mehta’s reply was: “Copies of Minutes of Board Meetings of the company for FY2016-17 are not available in our files, and we are unable to recall any such issue from memory. Please provide us with copies of Minutes and ledgers alluded to by you to enable us to comment appropriately.”

The forensic auditor found the response “we are unable to recall any such issue from memory” as a cover-up attempt. According to MSA, this went on to “demonstrate a very high possibility of the auditors concealing the true nature of the transactions and thereby giving vague replies to cover up their lapses”. It recommended a further detailed investigation.

The Blue Garden structure was key in the probe against Mankeshwar, too.

Sacked for directorships

Nagpur-based Ashwin Mankeshwar has had a colourful life for a chartered accountant. He has been, on occasions, seen on the city’s nascent Page 3 circuit and has had run-ins with a local politician over financial dealings. He was a director in Acton Global and Blue Garden Estates, the two special-purpose vehicles floated to enable a shady realty deal with Aditya Birla Finance between January and March 2017. It was the same financial year when loans of over INR390 crore from ABFL were routed through the two SPVs and onwards to BGPPL, an Avantha Group firm.

“Thus, Mr. Ashwin Mankeshwar himself having been a director in these two companies during a part of the financial year in which CG Power had entered into all the relevant transactions, should have had the knowledge about the transactions done by these companies with CG Power during FY2016-17. However, he has not flagged off any of these transactions in his Auditor’s Report of FY2017-18,” the forensic audit report said.

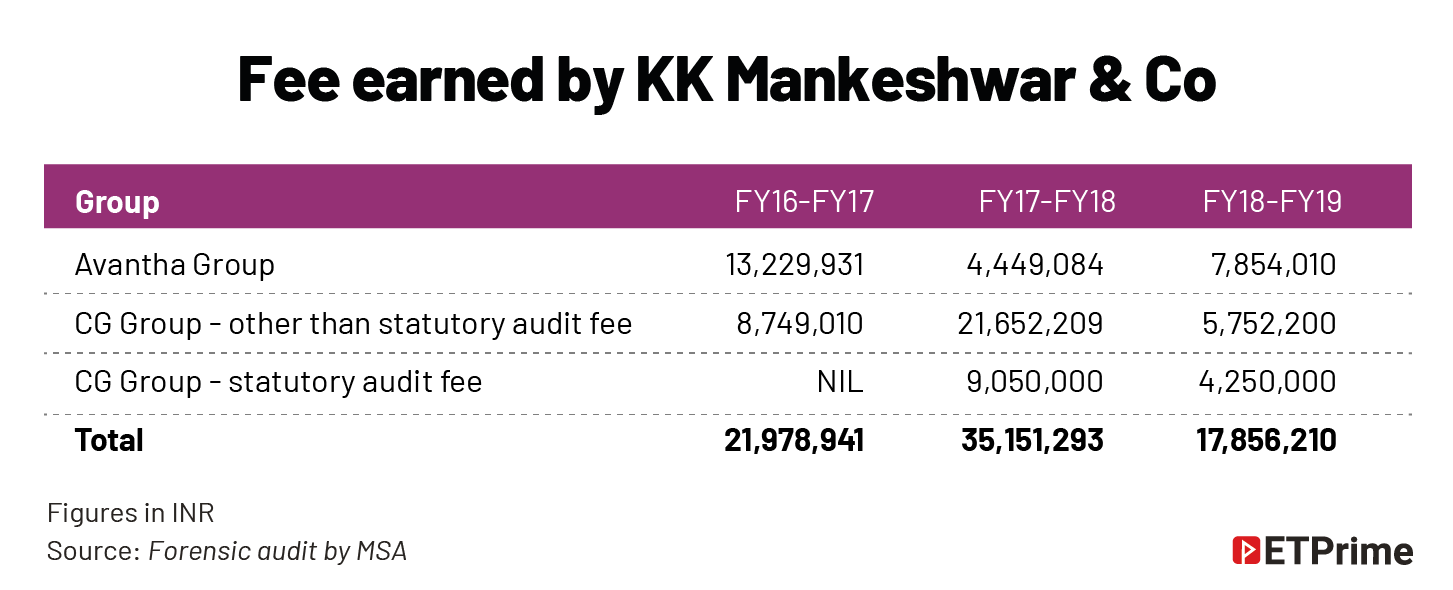

Also, the forensic auditor flagged the significant remuneration his firm received from CG Power and Avantha Group for other services. In FY17-18, when it received INR90.5 lakh as statutory audit fees from CG Power, it received more than INR2 crore for other services.

There were also inconsistencies between the nature of these expenses as was recorded in CG Power’s books and as reported by Mankeshwar to the forensic auditor. The forensic auditor found instances where expenses for services rendered to Avantha Holdings and BILT group were charged to CG Power.

In January 2020, the then board of directors of CG Power issued show-cause notice to KK Mankeshwar & Co (KKM). “Due to certain unexplained payments made to KKM as well as association of its partner with certain identified entities named in the Phase I investigation report, the Audit Committee issued a show-cause notice to KKM under Section 140(1) of the Companies Act. The Board determined that KKM cannot be independent, and decided to seek approval of the Central Government for the removal of KKM as Joint Statutory Auditor. KKM resigned as the Joint Statutory Auditors on 25 January 2020,” the company told its shareholders ahead of its annual general meeting in October 2020. But despite these findings, the latest show-cause notice issued by Sebi in May, did not include the audit firms or partners as noticees.

The red flags had started coming up when another auditor resigned much earlier.

Earlier resignation

Following the Sebi order banning PricewaterhouseCoopers in the Satyam matter, a spate of auditor resignations was reported in listed companies. Chaturvedi & Shah, which had taken up the joint audit mandate only the previous financial year, called it quits on April 27, 2018. This was the time when the accounts of FY18 were supposed to be audited. Did the firm quit as it sensed troubles ahead?

Remember, this was over a year before the stormy board meeting that saw the overthrowing of Thapar and the registrar of companies (RoC) getting concerned about the goings-on in the company.

When the RoC questioned the company, it informed that Chaturvedi & Shah “had to resign as statutory auditors of the company in order to fulfil a precondition for sanction of loan under consortium lending, which further required that the company has to engage a ‘Big Four’ Auditor as Statutory Auditor.”

But this did not convince the RoC, as only a month later, on May 29, 2018, the company appointed KK Mankeshwar & Co, which was not a Big Four firm, as auditor. The balance sheet of CG Power for FY18 was signed only by Mankeshwar.

In a report in November 2018, the RoC had recommended a probe into the books of accounts of the company under Section 206 and referred the matter to The Institute of Chartered Accountants of India (ICAI).

Further, an inspection by the regional director of companies was ordered. The inspection report submitted on September 23, 2019, a month after the infamous CG Power board meeting, said: “The basic trigger for conducting this inspection was the resignation of the statutory auditors of the company before the expiry of their tenure. This aspect has been reported in detail in the relevant paras in this Inspection Report with recommendations that the Ministry may consider referring the matter to NFRA/ICAI and other recommendations.”

These submissions were part of the corporate affairs ministry’s submission to the National Company Law Tribunal in a petition seeking restatement of accounts of CG Power. The petition was allowed in March 2020.

ICAI and the National Financial Reporting Authority (NFRA) are the watchdogs of the watchdogs. It is not clear whether the ministry has referred the matter to them, neither of which responded to ET Prime queries. Even if it had not, there is enough in the public domain for these agencies to take note and act.

But, like the dog in Doyle’s The Adventure of Silver Blaze, they seem to have done nothing yet.

(Graphics by Mohammad Arshad)