Clipped from: https://economictimes.indiatimes.com/markets/stocks/news/pnb-housings-wait-for-capital-gets-longer/articleshow/83902674.cmsSynopsis

The proposal to raise Rs 4,000 crore in a share sale structure that aimed to balance the need for funds to grow and overcome investment curbs faced by parent Punjab National Bank (PNB) is facing scrutiny on whether it ticks all the boxes on governance and legal compliance.

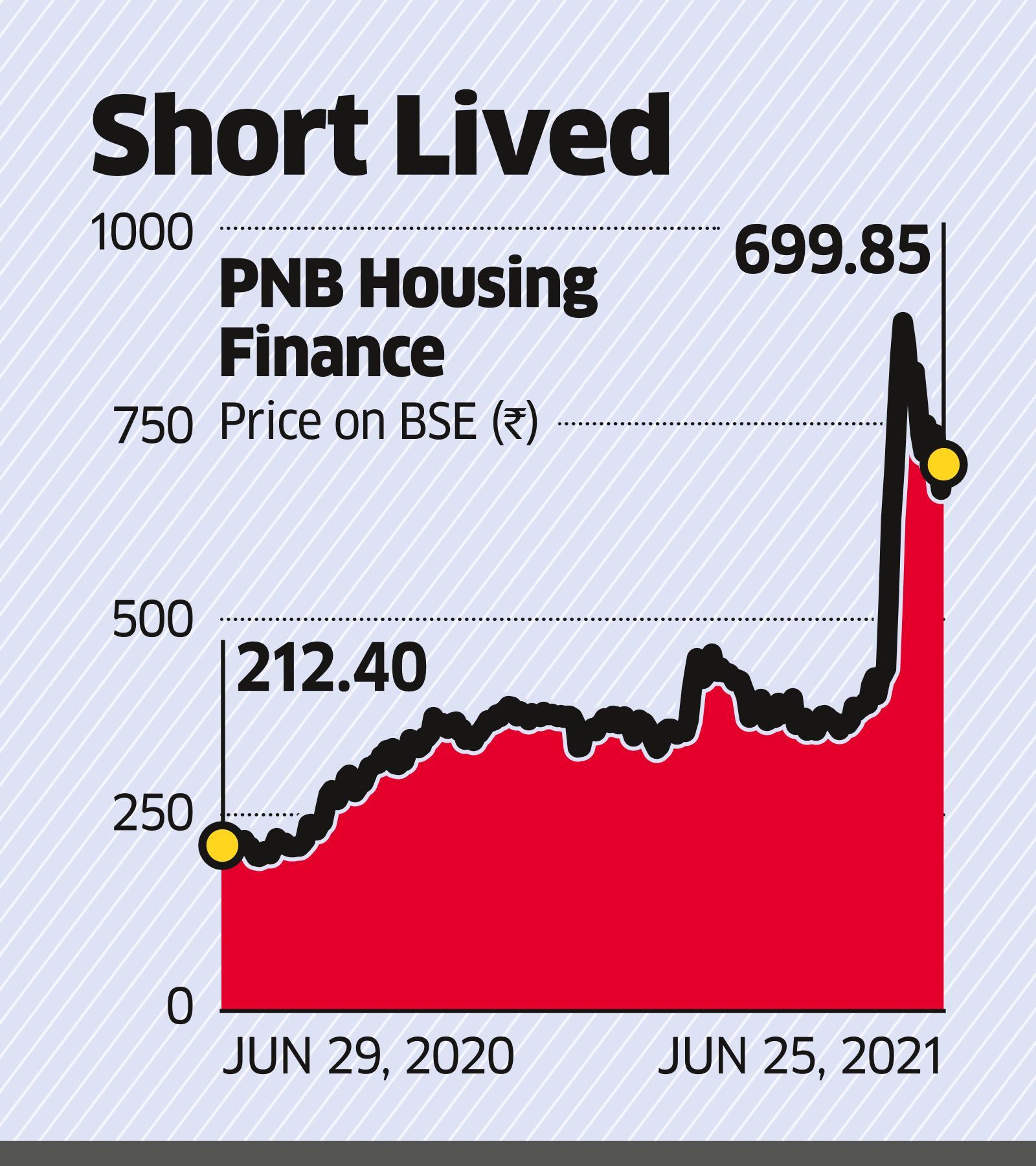

Mumbai | Kolkata: PNB Housing Finance’s two-year-long wait for capital was about to end this month. But uncertainty surrounds the fundraising plan as the mortgage lender battles allegations of short-changing minority investors and bypassing procedures to benefit a few.

The proposal to raise Rs 4,000 crore in a share sale structure that aimed to balance the need for funds to grow and overcome investment curbs faced by parentPunjab National BankNSE 1.89 % (PNB) is facing scrutiny on whether it ticks all the boxes on governance and legal compliance.

The board of PNB Housing on May 31 approved placement of 82 million preferential equity shares and 20.5 million share warrants with Pluto Investments, a Carlyle Group company, Salisbury Investments, the family investment vehicle of former HDFC Bank MD Aditya Puri, General Atlantic Singapore Fund FII and Alpha Investments V. Carlyle led the infusion with 80 per cent contribution.

Did you Know?

Stock score of Punjab National Bank moved up by 4 in a month on a 10-point scale.View Latest Stock Report »

At the heart of the dispute is whether funds could have been raised through a rights share issue and whether capital-starved promoter PNB has given away control to buyout firm Carlyle — without extracting a due premium. There is also the question of whether it complied with the need for an independent valuation, as prescribed by the Articles of Association (AoA).

While the Securities Appellate Tribunal (SAT) is set to rule on the dispute on July 5, experts say the circumstances determine the structure in such deals. It is all the more important in the light of the government and the Reserve Bank of India (RBI) directions on how the taxpayer-backed PNB utilises scarce capital.

The genesis of the capital raising tale goes back to July 2019 when the home financier’s board approved an equity raising of Rs 2,000 crore for the first time after its listing in 2016. PNB had initially decided against infusing capital, but had a change of heart in July 2020 and sought RBI’s nod to invest Rs 600 crore. But the central bank is said to have declined, likely due to the bank’s soaring bad loans and its failure to mobilise capital as planned.

“The refusal of permission forced PNB Housing to look outside for capital and Carlyle being an existing shareholder was a natural choice,” said a person familiar with the deal. Carlyle was also accompanied by its senior advisor and former HDFC Bank MD Aditya Puri, and that association boosted investor interest in the stock.

PNB Housing shares doubled to Rs 880 per share on June 7, from Rs 437 apiece on May 28, the day before the deal was announced. The stock surged 20 per cent on the day the deal was announced and continued to rise as traders priced in Carlyle’s deep pockets and Puri’s possible entry into the company.

“The fact that PNB could not invest meant it had to dilute its stake, which is what has happened. Everything was clear but the rise in PNB Housing’s share price made it look undervalued,” the person cited above said.

The stock has given up some gains due to the uncertainty over the fundraising. It ended at Rs 700 on Friday.

Proxy advisory firm Stakeholders Empowerment Services (SES) was the first to raise a red flag over the deal terming it legally non-compliant, with governance issues and fairness concerns. It asked investors to vote against the proposal.

The most critical point is the price at which Carlyle and Puri would be buying the shares of PNB Housing. While critics say it did not follow the AoA of the company, which prescribes independent valuation, those involved say it was done as per the formula prescribed by the markets regulator Sebi, which stands above the AoA. “While this is not required by law, the company has not disclosed if it has obtained such a valuation report,” said IiAS, a proxy advisor.

While it can be questioned from the governance point of view, it complies with the Sebi formula. The issue price of Rs 390 apiece is above the formula price of Rs 384.6.

The charge that not following AoA led to losses to minority shareholders too may not cut ice as the AoA talks only about valuation but does not prescribe the formula.