NBFCs can give dividend only if accounts are clean, NPAs not hidden, and are below 6 per cent for the last three years

The NPAs, satisfied by the RBI and auditors, have to be below 6 per cent for three consecutive years

The Reserve Bank of India (RBI) on Thursday tied down a non-banking financial company’s (NBFC’s) ability to pay dividends to certain factors, including how much bad debt it has in its books and whether it has declared it correctly.

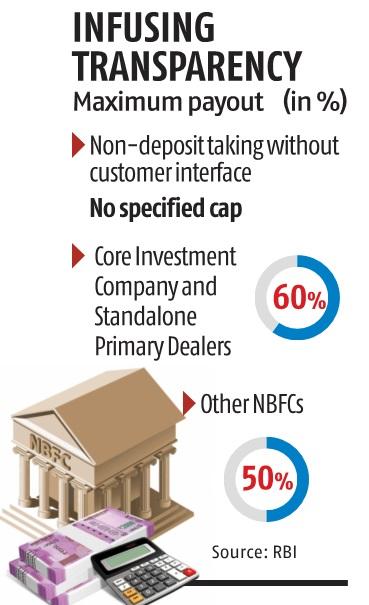

The dividend ratio, which is the ratio between the amount of the dividend payable in a year and net profit, is now capped at 50 to 60 per cent, depending upon the nature of the business. Any extraordinary income in the year has to be excluded from profits to arrive at the dividend ratio, the RBI said.

However, there will be no such cap on NBFCs that do not take public deposits and also do not have a customer interface. The RBI said the new norms would “infuse greater transparency and uniformity in practice.”

Before declaring the dividend, the board has to ensure that the regulator has not found any underreporting of non-performing assets (NPAs) by the NBFC. The NPAs, satisfied by the RBI and auditors, have to be below 6 per cent for three consecutive years. The NBFC should have the minimum capital adequacy ratio, which would be at least 15 per cent, in those three years. For standalone primary dealers, which deal in government business, the minimum capital adequacy will be 20 per cent.

Any NBFC that does not meet the criteria will also be eligible for dividend payout subject to a cap of 10 per cent. However, it must have a net NPA ratio of less than 4 per cent at the end of the financial year for which it is paying the dividend, the RBI said.

The auditors’ qualifications on the accounts and long-term growth plans of the NBFC have to be taken into consideration too before the board approves dividend, the RBI said. The dividend ratio has to be calculated on equity shares and compulsorily convertible preference shares that add up to the core capital.

“The Reserve Bank shall not entertain any request for ad-hoc dispensation on the declaration of dividends,” the central bank said.

NBFCs registered as a core investment company, which hold 90 per cent of its investment in group companies, can transfer dividends of up to 60 per cent. The same is the case for standalone primary dealers, while for the rest, which make up the bulk of the nearly 10,000 NBFC universe, the cap will be 50 per cent.

The tightening in dividend payout rules comes within a few weeks of the central bank’s norms on auditor appointments. NBFCs are against the auditor appointment move, but the central bank has remained adamant.

However, on the dividend payment front, there may not be much resistance, as there is no reason not to link dividends with future goals and having a clean account, experts say. It is a matter of hygiene for any firm, they say.

According to Jinay Gala, associate director at India Ratings, the tighter norms should not come as a burden for NBFCs.

“Most large firms meet prescribed norms for capital adequacy and bad loan ratio. They have improved provision cover for stressed assets plus many have raised capital during pandemic times,” Gala said, adding that the cap of 50 per cent on the dividend payout ratio is reasonable. Most NBFCs have a ratio below 40 per cent, he said.

A senior sector expert, who did not wish to be named, explained that the RBI has brought in the guidelines to harmonise the dividend payout rules for NBFCs. There are 11 kinds of NBFCs registered with the RBI, and each one has other sub categories. In total, there are nearly 10,000 NBFCs registered with the RBI. Every day, the central bank cancels some licences due to norm violations, and also gives fresh licences to others.

The dividend norms were not rationalised. For example, “housing finance companies did not have provision for dividend. Therefore, along the lines of banks, the circular for NBFCs has been issued,” said the sector expert.

The capital adequacy norms for each kind of NBFCs also vary. For example, gold loan companies must have tier-1 capital, or core capital, adequacy ratio of at least 12 per cent, which is higher than others’ 10 per cent. There are also varied restrictions on leverage. And so, harmonisation of rules is often difficult.