Select a dependent or person likely to shoulder family’s financial responsibilities

To avoid a dispute, one should name a nominee while purchasing the policy, or write a Will declaring the spouse as the nominee to the policy

The Madras High Court ruled in a recent case that a dependent wife did not have any legal claim to the life insurance proceeds from her husband’s death if the latter had not paid the policy premiums. In this case, the father-in-law had paid all the policy premiums. The deceased had not appointed a nominee for the policy, nor declared through a Will that his wife should receive the payout.

In the order, the judge wrote: “It is no doubt true that wife, mother and children are Class-I heirs of a male deceased, and not the father. But heirship will not be considered for this type of contingency, in case the entire contribution is not made by the deceased, and the same has been paid only by the father of the deceased.”

Explaining the rationale behind this decision, Vivek Sood, senior advocate in the Supreme Court, says: “Perhaps (subject to verification) what weighed with the Madras High Court was the fact that there was no nominee. The father having paid the premium would have a superior right over the legal heirs.” According to Sood, this view is debatable as it supersedes the law of succession and creates confusion about the concept of insurance.

Choose the right nominee

Many affluent parents pay the premium for insurance policies bought by their children to help the latter’s young family in the initial years. But if the son passes away and relations between the in-laws and the daughter-in-law sour, the latter could find herself in a soup, as happened in the Madras HC case.

To avoid a dispute, one should name a nominee while purchasing the policy, or write a Will declaring the spouse as the nominee to the policy.

Life insurance policies are bought to secure the lives of dependants and make up for financial loss suffered after the breadwinner’s demise. The nominee must be chosen carefully. Says Anup Seth, chief distribution officer, Edelweiss Tokio Life Insurance: “Assume you are the family’s primary income earner. Identify who will take over the financial responsibilities in your absence. In most cases, it is the spouse who is likely to do so. So, it is ideal to choose her/him as your nominee.”

Sometimes, a person may want the money to go to two parties, say, if he has a wife and minor child, and also a widowed mother. He could buy multiple policies and nominate the wife in one and his mother in the other. Alternatively, he could mention the share of the sum assured that should go to each of them. This point must be explained to the agent, distributor, or the life insurer’s representative clearly at the time of purchase. A written undertaking should be obtained from the insurer on this.

As for how to decide on splitting the sum assured among various nominees, Suresh Sadagopan, founder, Ladder7 Financial Advisories, says: “There is no fixed formula. Decide on the basis of love or principle of equity.”

If the nominee is a minor, choose a custodian to receive the amount on his/her behalf or else the claim process will not get initiated.

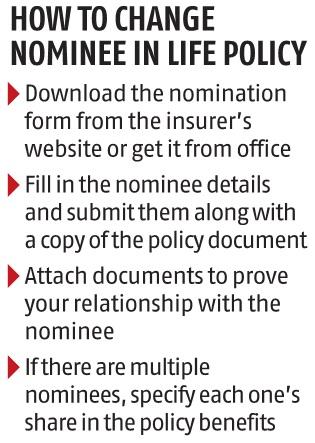

Changing the nominee

The nomination must be updated if the current nominee passes away. If this is not done, there could be complications at the time of claim settlement, especially if there are multiple legal heirs, or if the nominee was not a legal heir.

A change of circumstance can also warrant a change of nominee. Says Sadagopan: “A person may want to change the nominee when he gets married, divorced, remarried, has a child and wants to nominate it, or gets alienated from his spouse.” (See box: How to change nominee).