Synopsis–Rising commodity prices could begin squeezing the profitability of consumer companies. So far, companies have managed to pass on higher input costs to consumers without causing a big dent in volume growth but it may not go on for long.

Mumbai: Investor interest in an investment theme that has been the harbinger of optimism in Indian stocks for almost a decade might be running its course. The country’s top fund managers are increasingly baulking at shares of companies that benefited from India’s famed consumption story as growing pressures on profitability are raising questions about seemingly impregnable stock valuations.

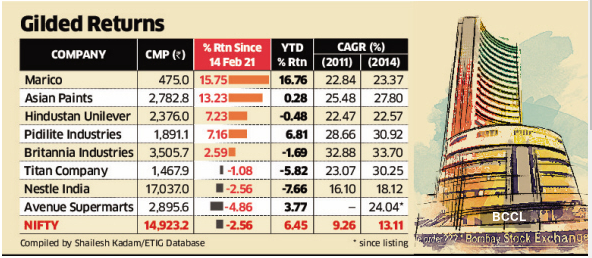

Top consumer stocks such as Hindustan Unilever, Nestle, Asian Paints, Titan and Avenue Supermarts among others have been missing in the monthly shopping lists of mutual funds for most of 2021. This is a sharp contrast to the situation earlier when fund managers could ill afford to keep these names out of the portfolio despite pricey valuations because these were among the handful of companies that were growing at a strong pace.

The tide has turned. With sectors such as metals, and cement making a strong comeback after almost 13 years of underperformance, thanks to the global upswing in commodity prices, consumer stocks have lost their allure.

“One of the reasons for the premium for consumer stocks was lack of earnings growth in many other sectors,” said Prashant Jain, chief investment officer, HDFC Mutual Fund. “With earnings growth becoming more broad-based, this could result in moderation of valuations for this sector.”

Rising commodity prices could begin squeezing the profitability of consumer companies. So far, companies have managed to pass on higher input costs to consumers without causing a big dent in volume growth but it may not go on for long.

Fund managers said the grimmer concern that firms face is that the second Covid wave, which has swept across rural India this time, unlike the initial surge in infections. With medical expenses shooting up, savings taking a hit and the government not in a position to spend its way out of a slowdown a second time after last year, consumption is unlikely to rebound at the same pace as it happened after infections subsided in 2020.

“Growth in the near term could moderate in this sector given the environment,” said Jain.

Firms might need to sacrifice record profit margins to maintain market share.

“Consumer companies have been enjoying high margins and rich valuations for a while,” said Anish Tawakley, senior fund manager and head of research, ICICI Prudential Mutual Fund. “Margins have been at their 15-year peaks, which are not sustainable.”

He likened this phase to the one in the late 1990s and early 2000s when margins and valuations were steep for consumer companies.

“These companies saw sharp EPS (earnings per share) cuts between 2000 and 2003,” he said. “We will be likely seeing a similar phase soon.”

That’s not good news for consumer stocks, which have moved from strength to strength in recent years because of profit growth. Since 2011, shares of Hindustan Unilever, Titan, Asian Paints, Pidlite and Nestle among others have returned between 16 per cent and 28 per cent on a compounded basis every year. In this period, an investor who put money in the benchmark Nifty would have got about 9 per cent at a compounded rate annually.

The near-uninterrupted advance in stock prices also meant steep share valuations. Fund managers said the valuations of Indian consumer companies are way higher than peers catering to a wider set of geographies. For instance, Nestle India trades at a price to earnings (PE) ratio — a popular valuation measure — of about 76 times, while its Swiss parent Nestle SA is at about 26 times. Similarly, Relaxo Footwear trades at a PE ratio of 95 times, while Wolverine World Wide, maker of the Hush Puppies brand, is at about 37 times.

“The sector per se will do well. If the economy grows at a nominal rate of 11 per cent, the sector will grow at 12-13 per cent, but the question is will this growth be enough to justify current valuations? My answer is no — current stock prices have built in much higher growth,” said Raamdeo Agrawal, chairman, Motilal Oswal Financial Services.

Fund managers will consider adding these stocks to their portfolios once the PE ratio shrinks.

“I would be comfortable taking a relook at consumer companies when their PE ratio falls below 40 times,” said Tawakley.

Share the joy of reading! Gift this story to your friends & peers with a personalized message. Gift Now