Regulator mulls replacing concept of ‘promoter’ with ‘person in control’

The regulator has said the definition of “promoter” is wide-ranging and needs to be revisited, with PE-backed companies increasingly looking to list | illustration: Ajay Mohanty

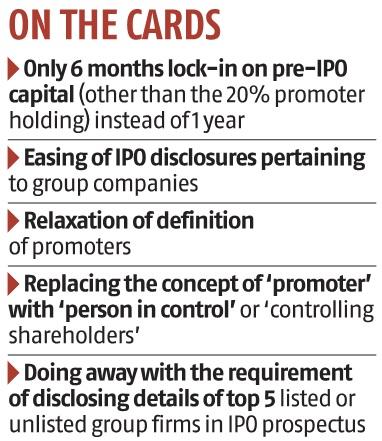

The Securities and Exchange Board of India (Sebi) on Tuesday proposed to liberalise the “Issue of Capital and Disclosure Requirements” (ICDR) by easing the lock-in period for promoters and rationalising the definition of “promoter group”. The proposals, if implemented, will ease the regulatory burden for listed firms and could encourage more companies to list.

The market regulator has said the three-year lock-in period promoters have to observe on at least 20 per cent of their shareholding after an initial public offering (IPO) can be brought down to one year.

Further, the lock-in requirement on promoter shareholding in excess of 20 per cent and pre-IPO non-promoter shareholding can be brought down from a year to six months.

Sebi said the lock-in requirement was necessary to ensure continuous “skin in the game”, particularly in the case of companies that were raising public capital for project financing or setting up greenfield projects. However, as most companies going public these days are “well established with mature businesses”, the condition can be done away with. Besides, greenfield financing through IPOs has become non-existent, the market regulator has said in a discussion paper. Experts said the move would help companies driven by private equity (PE).

“Typically, PE investors are glued to the business for five years or more before the company goes for listing. Their presence in the company’s management is a reflection of promoter commitment to the business, which is valued by the market as a whole. So enforcing a strict 20 per cent promoter shareholding lock-in for a significantly long period of three years was onerous, and it restricted promoters’ flexibility to optimise their shareholdings. The proposed changes shall bridge the gap,” said Prashaant Rajput, partner, White & Brief Advocates.

ALSO READ: Adani stocks dodge drop in Sensex, gain ahead of MSCI rebalancing

Sebi has proposed replacing the concept of “promoter” with “person in control”. The regulator has said the definition of “promoter” is wide-ranging and needs to be revisited, with PE-backed companies increasingly looking to list. Also, a lot of new-age and tech companies are not owned by families and do not have a distinctly identifiable promoter group.

“The changes in the nature of ownership could lead to situations where persons with no controlling rights and minority shareholding continue to be classified as promoter,” Sebi said.

It also sought public feedback on whether “the existing concept of promoter and promoter group should continue or there is a need to shift to the concept of ‘person in control’ or ‘controlling shareholders’ and ‘persons acting in concert’.”

Harish Kumar, partner, L&L Partners, said: “The shift from the concept of ‘promoter’ to ‘persons in control’ is likely to have a material impact on different regulations framed to govern family-driven businesses in India. Considering the continued subjectivity around the concept ‘control’, Sebi would have to work on clear guidelines to define that.”

Sebi has also proposed rationalising the definition of “promoter group” by dropping the clause which treated a group of individuals or companies holding 20 per cent or more stake in a company as promoter.

“Capturing the details of holdings by financial investors, while being a challenging task, may not result in any meaningful information to investors,” Sebi said.

The regulator has also proposed doing away with the requirement of disclosing financial and other details of the top five listed or unlisted group companies in the IPO prospectus.

Instead, only the names and registered office addresses of all the group companies should be disclosed in the offer document and other details can be made available on the websites of the listed companies.

Vidisha Krishan, partner at law firm MV Kini, said “such disclosures made the offer documents bulky and chasing after such entities prior to IPOs was a dead end task for most issuers”.