Clipped from: https://economictimes.indiatimes.com/wealth/tax/how-can-i-save-on-capital-gains-tax-from-sale-of-plot/articleshow/82291322.cmsSynopsis

The due date to invest in CGAS is 31 July 2021. Investments in post office time deposits are not eligible for the purpose of claiming exemption of capital gains.

ET Wealth’s panel of experts will answer questions related to any aspect of personal finance. If you have a query, mail it to us right away. Here is this week’s query on taxation from our readers.

I am 80. I bought a plot on the outskirts of Bengaluru for Rs 42,000 and the sale deed was registered in my wife’s name on 8 September 2004. My wife is 72. We have sold the plot and the sale deed was registered on 5 April this year for Rs 13 lakh. All payments were received by cheque. How do we save on capital gains tax? Can we deposit this amount in my post office senior citizens’ account for five years? My wife’s only source of income is the interest on FDs she receives from the bank, company and post office. We also purchased a flat worth Rs 69 lakh in January 2021. It is registered in the names of me, my wife and unmarried son. Will this purchase help with any deduction in capital gains tax?

Divakar Vijayasarathy, Founder and Managing Partner, DVS Advisors LLP, replies: The resultant capital gains in the hands of your wife from the sale of the plot will be Rs 11,88,124. This gain can be mitigated by investing in a residential property a year before or two years after the sale of the site. The amount invested in the flat bought in 2021 shall be allowed as an exemption for capital gains. However, as the property was purchased in three names, the exemption amount shall be distributed and Rs 23 lakh will be available to your wife to claim as exemption. For the purpose of claiming the exemption, your wife should not own more than one residential property, apart from the one purchased this year. If your wife owns more property, or the share of Rs 23 lakh has already been claimed as an exemption, then there is an option of investing in the Capital Gains Account Scheme. The due date to invest in CGAS is 31 July 2021. Investments in post office time deposits are not eligible for the purpose of claiming exemption of capital gains.

Read More News on

capital gains taxinvestCGASpropertycapital gains tax exemptionincome taxTaxmanaging partnertaxationcapital gains(Click here to know how to save on taxes for the financial year 2020-21.)

Download The Economic Times News App to get Daily Market Updates & Live Business News.NEXT STORYAdvertorial

Are you really saving your taxes? Know your Tax slabs & review your investment plans now!

It’s that time of the year again, when our investments come again to the forefront. The investment receipts are all out, our inbox is full of mails urging us to claim our tax-saving investments and most of us are once again struggling to check if our investments are enough. The tax-filing season in India begins in early January and our last minute investments continue to be made for as long as March. While the tax-paying population in India is on the lower side, the income tax collection during 2018-19 amounted to ₹ 442,170 crore. This leads us to the important question – Is our investment plan doing the best for our current tax slabs?

This question is bound to torment you every tax-filing season. But with the right information, you can easily make investments that pay off. The first thing you need to ensure is that you have a portfolio that is tailored to cater to your taxability and you need to have a basic understanding of the various income tax slabs. If you are in the middle of the tax-pool, in the 20% bucket, chances are it may be easy for you to save taxes with some simple steps. However, it becomes very challenging if you belong to the higher tax bracket of 30%! And if you too are wondering how your investment plans currently fare, here’s what you need to know!

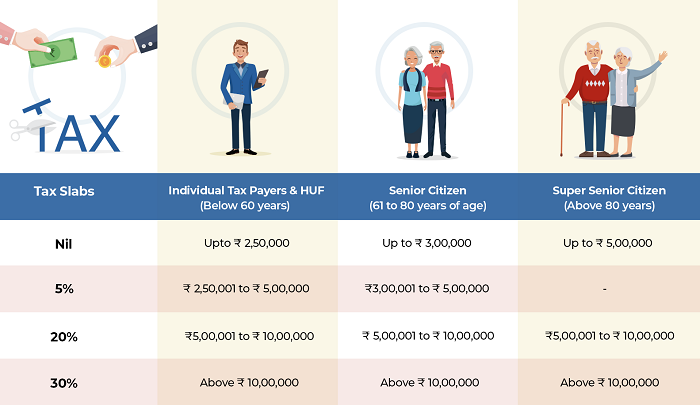

But first, check your tax slabs based on your taxable income –

There is an additional 4% Health & Education Cess that needs to be paid on every front.

In addition to this, people with a taxable income bracket of up to ₹ 5,00,000 also need to note that they are eligible for full tax rebate. This change, which was announced in last year’s Union Budget is a silver-lining for many who are looking to fully utilize their tax-benefits.

Now that you know your tax slab, the next step is to plan your investments depending on your lifestyle. Whether you are a single person keen on experiencing the different things in life, or a happily married couple planning for kids, there are some simple investment switches that you can make to ensure that your life-goals are never out of reach. This is especially true since the various aspects of saving taxes are far too diverse. From your home loan EMIs to your children’s tuition fee, there are tax exemptions for a variety of different things that you can benefit from. Here’s the area that you need to check –

For single folks busy exploring life

If you are one from the clan of wanders & explorers & are keen on travelling the world to find your own path, then ‘investments’ may very well be the ‘road not taken’. However, if you give it a thought, now seems to be a good time for you to consider a few investments that will come in handy for your future travels. If you already bear an education loan, then turning towards a trust-worthy life insurance plan is a must. The interest paid on your education loan in itself will bear you tax benefits under section 80E of the Income Tax Act. In addition to this, opting for a ULIP (Unit Linked Insurance Plan) can also help you fulfill all your aspirations. ULIP options like the HDFC Life Click 2 Wealth plan are a brilliant way of investing in market-linked instruments while curtailing the risk that normally accompanies it. The Invest Plus option of HDFC Life Click 2 Wealth Plan provides a life insurance while also taking care of your investment needs by providing accumulated fund value at the time of maturity.

In addition to this basic benefit, such investment plans in themselves help you save up to ₹ 1.5 lakhs. Under Section 80C of the Income Tax Act, the premium you pay towards these schemes offer tax-deduction. In addition to this, you can also consider a health insurance plan to claim deductions of up to ₹ 25,000 under Section 80D. The fact that the premiums for life insurance and health insurance are lower if you apply at a younger age is bound to be an added benefit.

Investments to consider – Life Insurance, ULIP, Health Insurance.

The Happily Married Couple

If you are a happily married person, either planning to have kids or already have kids, then you need to ensure that these factors are accounted for in your investments as well! Your home loans, personal health insurance and life insurance plans might help you save over ₹ 20000, ₹ 88000 or ₹ 100000, in total, based on your tax slabs*. However, it is always advisable to recheck these investments to ensure your partners are also well-covered.

One such plan, trusted by investment advisors through and through is HDFC Life Click 2 Protect 3D Plus. The online term insurance plan not only has our back in case of an uncertainty (death), but also offers support to tackle certain disease and even disability. With a claim settlement ratio of 99.03% for 2018-19, HDFC Life Click 2 Protect 3D Plus offers benefits like whole life cover, life stage protection feature, premium waiver benefit, tax benefits as per prevailing tax laws and more.

If you still feel like you are shelling out more to taxes, turning to instruments like the National Pension Scheme, which offers an additional deduction for investment up to Rs. 50,000 in NPS is available exclusively under subsection 80CCD (1B); is a great means of adding to your tax-savings while also planning your retirement!

Investments to Consider: National Pension Scheme, Family Floater Health Insurance, Life Insurance with Premium Waiver Benefits.

Etching towards retirement

If you are reaching closer to your retirement age, chances are the bigger chunks of your life-goals are already achieved. The home-loan is reaching its last leg of EMIs or already paid off, the alternate income options like stocks, mutual funds or even a small-scale business are already set up, but the tax-saving options may seem to be minimal. However, this is the perfect time to increase your contribution to your provident fund, and also focus more on contributing to the voluntary EPF fund.

Your investment to the EPF scheme, home loan payments, and life insurance premiums will help you enjoy the complete benefits of Section 80C. In addition to this, you could relook on your investment portfolio and financial strategy and add in a trusted Guaranteed Savings plan, which will further cushion your retirement plans! One such plan is HDFC Life Sanchay Plus, which offers guaranteed returns to you and your family.

HDFC Life Sanchay Plus not only gives us a guaranteed return in either lump-sum or regular monthly incomes, but also offers Life Long Income option (Guaranteed Income till age 99 years) provided all due premiums have been paid and the policy is in force. This plan option also offers return of your premium at the end of the payout period. Now is also a great time to re-evaluate the Health Insurance Plans for you and your family to avail all deductions of up to ₹ 50,000 under Section 80D.

Investments to Consider: Review your health insurance plan, Guaranteed Savings Plan, Increase your contributions to PF and EPF.

The Wise Retired Ones!

The tax-benefits that you enjoy once you are into retirement and in the senior-citizen club are unique and quite beneficial to all. You can enjoy tax-free income of up to ₹ 5,00,000 (based on tax-slab eligibility), your investment kitty opens up for new and better investments to further save taxes and the repayments from your retirement plans during your corporate tenure will help you truly enjoy life. With most responsibilities off your shoulders, you can focus on shifting your investments towards products like Senior Citizen Savings Scheme, National Savings Certificates, ELSS, etc.

In addition to this, retired people can also ensure a regular income option by buying an annuity plan like the HDFC Life Pension Guaranteed Plan, which provides guaranteed regular income for lifetime. HDFC Life Pension Guaranteed Plan is a single premium annuity product, designed to cater your needs. You can either take a single or joint life plan and you have the option of receiving immediate or deferred annuity.

Investments to Consider – Senior Citizen Savings Scheme, National Savings Certificates, Annuity Plan

There is no questioning the fact that there is a financial plan that suits your ask and caters to what you need in every stage of life. So whether you are new to the corporate world, still trying to figure out your financial plan or happily retired, recheck your investment portfolio and ask yourself – are you really saving your taxes?