Clipped from: https://taxguru.in/goods-and-service-tax/liability-pay-cases-cgst-act-2017.html

Liability to pay in certain cases under Central Goods and Services Tax (CGST) Act, 2017

Chapter XVI of the Central Goods and Services Tax Act, 2017 deals with liability to pay tax in certain cases, where an amount is due under the GST regime (Tax, Interest, and Penalty) which cannot be recovered from the taxpayer directly.

Post Covid-19 pandemic, it has been noticed that major corporate houses have gone for corporate restructuring to sustain their business activity whereas non-corporate persons struggled to sustain. In such scenario, where the businesses were hampered a lot and there is no sign of recovery, this has led to some business arrangements in both corporate and non-corporate sectors which results in imposition of liability to pay tax, interest and penalty under the following circumstances.

| CORPORATE SECTOR | NON CORPORATE SECTOR |

| Liability arising before and after transfer of business in Whole or in part. | Liability arising upon death of proprietor, where business is continued by legal heir or otherwise discontinued or where change in constitution of business occurs. |

| Merger and amalgamation of two or more corporate entityin pursuance of court/tribunal order. | Liability upon Guardian, Trustee and agent where business is run on behalf of a minor or an incapacitated person. |

| Winding up of company in pursuance of court/tribunal order or otherwise. | Where an estate under dispute is controlled by the Court of wards |

| Liability upon Company and its Directors to pay tax, interest and penalty | Liability upon Firm and its partners to pay tax, interest and penalty |

| Liability in case of conversion of Private company to a Public company, LLP | Partition of Property of HUF/AOP. |

| Dissolution of Partnership firm or termination of Guardianship or Trust | |

| Where an agent supplies or receives taxable goods on behalf of its principal |

Section 85 read with Rule 19 of the CGST Rules, 2017:

Liability in case of transfer of business

This section deals with liability to pay tax in case of transfer of business under following circumstances:

- Liability arising before transfer of business either wholly or in part by way of Sale, Gift, Lease, Leave and License, Hire or in any other manner whatsoever, both transferor and transferee will be jointly and severally liable, either wholly or to the extent of such transfer for payment of taxes, interest or penalty whether such tax, interest or penalty has been determined before or after such transfer, but has remained unpaid.

In the event of death of a business proprietor, two situations may commonly arise:

i. Business is continued by Legal heir – Where business is decided to be continued by his successor or transferee, the following procedure gives a brief idea about such transfer.

Application for Registration

The applicant shall file Form GST REG-01 and mention the reason for obtaining such registration as ‘Death of Proprietor’. Death certificate of the deceased person is required to be uploaded along all other necessary documents.

⇓

Transfer of ITC

Sec. 18(3) r.w. Rule 41 of the CGST Rules allows the transfer of unutilized ITC lying in the electronic credit ledger over to the transferee. The transferor shall submit Form GST ITC-02 which shall be accepted by the transferee. A certificate by a Chartered Accountant is to be affixed along with the form. The ITC shall be transferred immediately as soon as the transferee accepts such form.

⇓

Application for cancellation of Registration

Incase of death of sole proprietor of a business concern, the legal heir may file an application for cancellation of registration in Form GST REG-16, along with details of inputs held in stocks or inputs sustained in semi-finished or finished goods as on the date from which the cancellation of registration is sought, along with the details of the payment, if any, made against any liability and also furnish relevant documents within 30 days of the occurrence of the event warranting the cancellation, either directly or through a Facilitation Centre notified by the Commissioner.

⇓

Transfer of additional liability

In case a transferor being the sole proprietor of a business dies, the liability to pay any tax, interest or penalty due from the transferor, incase of business being transferred in whole or in part, shall be cleared by the transferee or successor.

⇓

ii. Business is discontinued by Legal heir – Where business is decided to be discontinued, the following procedure gives a brief idea about such discontinuance.

Remittance of tax and cancellation of registration

Section 29(5) r.w. Rule 20 of the CGST Rules, any taxpayer seeking cancellation of registration shall pay ITC contained in the stock of inputs, semi-finished goods, finished goods and capital goods or the output tax payable on such goods, whichever is higher, by debiting either electronic cash or credit. Form GSTR-10 is required to be filed for cancellation of registration within 3 months from the date of cancellation or date of cancellation order, whichever is later. Incase Form GSTR-10 is not filed within stipulated date, notice in Form GSTR-3A shall be issued to the taxpayer. If the taxpayer still fails to file the return within 15 days of the receipt of notice, an assessment order in Form GST ASMT-13 shall be issued to determine the tax liability of the taxpayer. Upon payment of taxes within 30 days of receipt of such order, the case shall be deemed to have been withdrawn. However, liability to pay interest and late fee shall continue.

⇓

Liability to pay

Where the business is carried on by the person is discontinued, whether before or after his death his legal representative shall be liable to pay, out of the estate of the deceased, to the extent to which the estate is capable of meeting the charge, the tax, interest or penalty due from such person under this act, whether such tax, interest or penalty has been determined before his death but has remained unpaid or is determined after his death.

- Liability arises after transfer of business where the transferee carries on such business either in his own name or in some other name is liable to pay tax on supply of goods or services or both effected by him w.e.f. such transfer. The transferee shall be liable to apply for amendment of his certificate of registration within 15 days of such change, duly signed or verified through electronic verification code, in Form GST REG-14, along with documents, either directly or through a Facilitation Centre notified by the Commissioner.

In case the change relates to –

a. Legal name of business.

b. Address of the principal place of business or any additional place(s) of business

Addition, Deletion or retirement of partners or directors, Karta, Managing Committee, Board of Trustees, Chief Executive Officer or equivalent, responsible for the day to day affairs of the business,which does not warrant cancellation of registration, the proper officer shall after due verification, approve the amendment within 15 working days and issue an order in Form GST REG-15 and such amendment shall take effect from the date of occurrence of the event warranting such amendment.

- In case a business in its entirety is being sold as a ‘going concern’, commonly known as ‘Lock, Stock, Barrel basis’, such sale is not taxable as per para 4(c) of Schedule II of the CGST Act read with exemption notification no. 12/2017 dated 28.06.2017.

Certification by Chartered Accountant/ Cost Accountant

Several provisions under GST require certification by a Chartered Accountant/ Cost Accountant in the areas given below:

Certificate under Sec. 18(1)(a) r.w. Rule 40(1)(d) of CGST Rules, 2017

A person who has applied for registration under CGST/SGST Act within 30 days from the date on which he becomes liable to registration and has been granted such registration shall be entitled to take ITC in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock on the day immediately preceding the date from which he becomes liable to pay tax under the SGST/CGST Act, 2017 by declaring the same, electronically, on the common portal in Form GST ITC-01.

Where aggregate claim exceeds Rs. 2Lakh, a certificate from Practicing Chartered Accountant/Cost Accountant shall be submitted.

Certificate under Sec. 18(1)(b) r.w. Rule 40(1)(d) of CGST Rules, 2017

A tax payer who takes voluntary registration under section 25(3) of the CGST Act and SGST Act, is eligible to avail ITC in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock on the day immediately preceding the date of grant of registration by declaring the same, electronically, on the common portal in Form GST ITC-01

Where aggregate claim exceeds Rs. 2Lakh, a certificate from Practicing Chartered Accountant/Cost Accountant shall be submitted.

Certificate under Sec. 18(1)(c) r.w. Rule 40(1)(d) of CGST Rules, 2017

When any registered person ceases to pay tax for Composition scheme under section 10, he is eligible to avail Input Tax Credit in respect of inputs held in stock, inputs contained in semi-finished or finished goods held in stock and on capital goods (as reduced by the prescribed percentage points) on the day immediately preceding the date from which he becomes liable to pay tax u/s 9 of the CGST / SGST Acts, 2017, by declaring the same, electronically, on the common portal in Form GST ITC-01.

Where aggregate claim exceeds Rs. 2Lakh, a certificate from Practicing Chartered Accountant/Cost Accountant shall be submitted.

Certificate under Sec. 18(1)(d) r.w. Rule 40(1)(d) of CGST Rules, 2017

Where an exempt supply by a registered person becomes taxable supply, the registered person is eligible to avail Input Tax Credit in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock relatable to such exempt supplies and on capital goods (as reduced by the prescribed percentage points) exclusively used for such exempt supplies on the day immediately preceding the date on which such exempt supplies become taxable supplies under the CGST / SGST Acts, 2017 by declaring the same, electronically, on the common portal in Form GST ITC-01.

Where aggregate claim exceeds Rs. 2Lakh, a certificate from Practicing Chartered Accountant/Cost Accountant shall be submitted.

Certificate under Sec. 18(3) r.w. Rule 41(2) of CGST Rules, 2017

Where there is a change in the constitution of a registered person on account of sale, merger, demerger, amalgamation, lease or transfer of the business with the specific provisions for transfer of liabilities, the said registered person shall be allowed to transfer the input tax credit which remains un-utilized in his electronic credit ledger to such sold, merged, demerged, amalgamated, leased or transferred business in the manner prescribed in the CGST/SGST Rules, 2017 by declaring the same, electronically, on the common portal in Form GST ITC-02.

Certificate is duly issued by a Chartered Accountant/Cost Accountant in respect of a person who has sold/merged/de-merged/amalgamated/leased/ transferred its business with a specific provision for the transfer of liabilities.

Certificate under Sec. 18(4) r.w. Rule 44(5) of CGST Rules, 2017 – Composite Taxpayer

Where the applicant who has availed ITC opts to pay tax under Section 10 of the CGST and SGST Acts, shall be liable to pay an amount, by way of debit in the electronic credit ledger or electronic cash ledger, equivalent to the credit of input tax in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock on the day immediately preceding the date of exercising the option to pay tax u/s 9 of the CGST / SGST Acts, 2017, as on date by declaring the same, electronically, on the common portal in Form GST ITC-03.

The details so furnished in the above statement shall be duly certified by a practicing Chartered Accountant or a Cost Accountant.

Certificate under Sec. 18(4) r.w. Rule 44(5) of CGST Rules, 2017 – Taxable supplies by Registered person become wholly exempt

Where a taxable supply by a registered person becomes exempt supply the applicant who has availed ITC, shall be liable to pay an amount, by way of debit in the electronic credit ledger or electronic cash ledger, equivalent to the credit of input tax in respect of inputs held in stock, inputs contained in semi-finished or finished goods held in stock and on capital goods used for such taxable supplies on the day immediately preceding the date on which such taxable supplies become exempt supplies under the CGST / SGST Acts, 2017 by declaring the same, electronically, on the common portal in Form GST ITC-03.

The details so furnished in the above statement shall be duly certified by a practicing Chartered Accountant or a Cost Accountant.

Certificate under Sec. 29(5) r.w. Rule 44(5) of CGST Rules, 2017

Where every registered person whose registration is cancelled shall pay an amount, by way of debit in the electronic credit ledger or electronic cash ledger, equivalent to the credit of input tax in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock or capital goods or plant and machinery on the day immediately preceding the date of such cancellation or the output tax payable on such goods, whichever is higher under the CGST/SGST Act, 2017 by declaring the same, electronically, on the common portal in Form GSTR-10.

The details so furnished in the above statement shall be duly certified by a practicing chartered accountant or a cost accountant.

Certificate under Sec. 54 r.w. Rule 89 of CGST Rules, 2017

Where the applicant has filed an application for refund u/s 54 of the CGST / SGST Act, 2017 under the following scenario:

- Refund of tax paid on zero-rated supplies export of goods or services or both or on inputs or input services used in making such zero-rated supplies exports; *

- Refund of unutilised input tax credit under sub-section (3); *

- Refund of tax paid on a supply which is not provided, either wholly or partially, and for which invoice has not been issued, or where a refund voucher has been issued; *

- Refund of tax in pursuance of section 77; *

- The tax and interest, if any, or any other amount is paid by the applicant and he has not passed on the incidence of such tax and interest to any other person; *[strike whichever is not applicable]

Where incidence of tax, interest or any other amount claimed as refund, in the application for refund has not been passed on to any other person, in a case where the amount of refund claimed exceeds Rs. 2Lakh.

Certificate under Notification dated 05.10.2017 issued by DIPP- Eligible unit has not received any inputs from another business premises

Where the eligible unit is entitled for budgetary support on manufacture of specified goods which shall be sum total of

(i) 58% of the Central tax paid through debit in the cash ledger account maintained by the unit in terms of section 49(1) the CGST Act, 2017 after utilization of the ITC of the Central Tax and Integrated Tax.

(ii) 29% of the integrated tax paid through debit in the cash ledger account maintained by the unit in terms of section 20 of the IGST Act, 2017 after utilization of the ITC Tax of the Central Tax and Integrated Tax.

The details so furnished shall be duly certified by a practicing Chartered Accountant or a Cost Accountant at specific request of the company for submission with GST department.

Certificate under Notification dated 05.10.2017 issued by DIPP- Eligible unit has received any inputs from another business premises

Where the eligible unit is entitled for budgetary support on manufacture of specified goods which shall be sum total of

(i) 58% of the Central tax paid through debit in the cash ledger account maintained by the unit in terms of section 49(1) the CGST Act, 2017 after utilization of the ITC of the Central Tax and Integrated Tax.

(ii) 29% of the integrated tax paid through debit in the cash ledger account maintained by the unit in terms of section 20 of the IGST Act, 2017 after utilization of the ITC Tax of the Central Tax and Integrated Tax.

The details so furnished shall be duly certified by a practicing Chartered Accountant or a Cost Accountant at specific request of the company for submission with GST department.

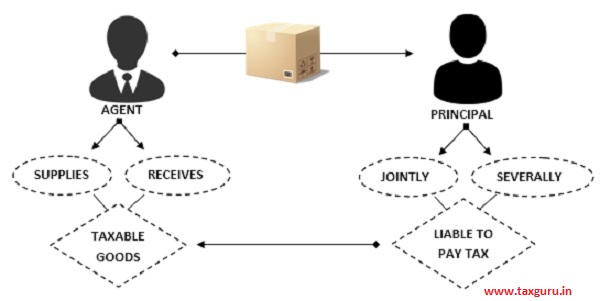

Section 86: Liability of Agent and Principal

Where an agent supplies or receives any taxable goods on behalf of his principal, such agent and his principal shall, jointly and severally, be liable to pay the tax payable on such goods under this Act.

Section 87: Liability in case of amalgamation or merger of companies

- When 2 or more companies are amalgamated or merged in pursuance of an order of court or of Tribunal or otherwise and the order is to take effect from a date earlier to the date of the order and any two or more of such companies have supplied or received any goods or services or both to or from each other during the period commencing on the date from which the order takes effect till the date of the order, then such transactions of supply and receipt shall be included in the turnover of supply or receipt of the respective companies and they shall be liable to pay tax accordingly.

- Notwithstanding anything contained in the said order, for the purposes of this Act, the said two or more companies shall be treated as distinct companies for the period up to the date of the said order and the registration certificates of the said companies shall be cancelled with effect from the date of the said order.

Analysis: Where date of order of NCLT is on a later date than the effective date of merger given in the order, then such intermediate supply of goods or services or both shall be taxable in the hands of the respective companies. The two companies shall be treated as a single company w.e.f. the date of order of NCLT.

> Effective order date: 01-06-2019

> Order issue date: 20-07-2019

(Intermediate supply of goods or services between 01-06-2019 to 20-07-2019 shall be taxable separately in the hands of respective companies)

Section 88 read with Rule 160 of theCGST Rules, 2017:

Liability in case of Company in Liquidation

- When any company is being wound up whether under the orders of a court or Tribunal or otherwise, every person appointed as receiver of any assets of a company (hereafter in this section referred to as the “liquidator”), shall, within 30 days after his appointment, give intimation of his appointment to the Commissioner.

- The Commissioner shall, after making such inquiry or calling for such information as he may deem fit, notify the liquidator within three months from the date on which he receives intimation of the appointment of the liquidator, the amount which in the opinion of the Commissioner would be sufficient to provide for any tax, interest or penalty which is then, or is likely thereafter to become, payable by the company. The intimation must be sent in Form GST DRC-24 to the liquidator. This intimation must contain the following details:

a) Name of the company being liquidated

b) The GSTIN of the company being liquidated

c) Date of the letter

d) Period for which demand is being made

e) Demand Order No.

f) Reference to Liquidator’s letter intimating liquidation of the company

g) The actual amount or likely amount, the company owes to State/ Central Government in terms of tax, interest, penalty, other dues and total arrears thereof

- When any private company is wound up and any tax, interest or penalty determined under this Act on the company for any period, whether before or in the course of or after its liquidation, cannot be recovered, then every person who was a director of such company at any time during the period for which the tax was due shall, jointly and severally, be liable for the payment of such tax, interest or penalty, unless he proves to the satisfaction of the Commissioner that such non-recovery cannot be attributed to any gross neglect, misfeasance or breach of duty on his part in relation to the affairs of the company.

Analysis: A company in winding up shall appoint a Liquidator who shall intimate the Commissioner of his appointment within 30 days. The Commissioner shall notify the liquidator for recovery of any amount representing tax, interest, penalty, or any other amount due in Form GST DRC-24. In case a private company is being wound up and any tax, interest or penalty cannot be recovered, then every director during which such tax is or was pending shall be jointly and severally liable for payment unless he proves contrary to the Commissioner.

Section 89: Liability of Directors of Private Company

- Notwithstanding anything contained in the Companies Act, 2013 (18 of 2013), where any tax, interest or penalty due from a private company in respect of any supply of goods or services or both for any period cannot be recovered, then, every person who was a director of the private company during such period shall, jointly and severally, be liable for the payment of such tax, interest or penalty unless he proves that the non-recovery cannot be attributed to any gross neglect, misfeasance or breach of duty on his part in relation to the affairs of the company.

- Where a private company is converted into a public company and the tax, interest or penalty in respect of any supply of goods or services or both for any period during which such company was a private company cannot be recovered before such conversion, then, nothing contained in sub-section (1) shall apply to any person who was a director of such private company in relation to any tax, interest or penalty in respect of such supply of goods or services or both of such private company:

Provided that nothing contained in this sub-section shall apply to any personal penalty imposed on such director.

Analysis: Where a Private company fails to pay any tax, interest or penalty,then every director during which such tax is or was pending shall be jointly and severally liable for payment unless he proves contrary. Whereas, if a private company converts into a public company and any tax remains pending before such conversion, such directors shall not remain liable unless any personal penalty is imposed on such director.

Section 90: Liability of Partners of firm to pay tax

- Notwithstanding any contract to the contrary and any other law for the time being in force, where any firm is liable to pay any tax, interest or penalty under this Act, the firm and each of the partners of the firm shall, jointly and severally, be liable for such payment:

Provided that where any partner retires from the firm, he or the firm, shall intimate the date of retirement of the said partner to the Commissioner by a notice in that behalf in writing and such partner shall be liable to pay tax, interest or penalty due up to the date of his retirement whether determined or not, on that date:

Provided further that if no such intimation is given within one month from the date of retirement, the liability of such partner under the first proviso shall continue until the date on which such intimation is received by the Commissioner.

Analysis: Where a Firm fails to pay any tax, interest or penalty, then every firm and each of the partners during which such tax is or was pending shall be jointly and severally liable for payment. In case where any partner resigns, he shall intimate in writing to the Commissioner the date of retirement, then he shall be held liable till the date of his retirement. However, if such intimation is not provided within 30 days, liability of such partner shall continue until the commissioner receives such intimation.

Section 91: Liability of guardians, trustees

- Where the business in respect of which any tax, interest or penalty is payable under this Act is carried on by any guardian, trustee or agent of a minor or other incapacitated person on behalf of and for the benefit of such minor or other incapacitated person, the tax, interest or penalty shall be levied upon and recoverable from such guardian, trustee or agent in like manner and to the same extent as it would be determined and recoverable from any such minor or other incapacitated person, as if he were a major or capacitated person and as if he were conducting the business himself, and all the provisions of this Act or the rules made thereunder shall apply accordingly.

Analysis: Where a business held by a guardian, trustee or agent of a minor or incapacitated person fails to pay any tax, interest or penalty, then it will be recovered from such guardian, trustee or agent.

Section 92: Liability of court of wards

Where the estate or any portion of the estate of a taxable person owning a business in respect of which any tax, interest or penalty is payable under this Act is under the control of the Court of Wards, the Administrator General, the Official Trustee or any receiver or manager (including any person, whatever be his designation, who in fact manages the business) appointed by or under any order of a court, the tax, interest or penalty shall be levied upon and be recoverable from such Court of Wards, Administrator General, Official Trustee, receiver or manager in like manner and to the same extent as it would be determined and be recoverable from the taxable person as if he were conducting the business himself, and all the provisions of this Act or the rules made thereunder shall apply accordingly.

Analysis: Where an estate (either partly or wholly) held by a Court of Wards, the Administrator General, the Official Trustee or any receiver or managerappointed by or under any order of a court fails to pay any tax, interest or penalty, then it will be recovered from such persons.

Section 93: Special provisions regarding liability to pay tax, interest or penalty in certain cases

- Save as otherwise provided in The Insolvency and Bankruptcy Code 2016, where a person, liable to pay tax, interest or penalty under this act, dies, then –

a) if a business is carried on by the person is continued after his death by his legal representative or any other person, such legal representative or other person, shall be liable to pay tax, interest or penalty due from such person under this act; and

b) if the business is carried on by the person is discontinued, whether before or after his death his legal representative shall be liable to pay, out of the estate of the deceased, to the extent to which the estate is capable of meeting the charge, the tax, interest or penalty due from such person under this act, whether such tax, interest or penalty has been determined before his death but has remained unpaid or is determined after his death.

- Save as otherwise provided in the Insolvency and bankruptcy Code 2016, where a taxable person, liable to pay tax, interest or penalty under this act, is a Hindu Undivided Family or an Association of Persons and the property of the Hindu undivided family or Association of Person is partitioned amongst the various members or groups of members, then, each member or group of members shall, jointly and severally, be liable to pay the tax, interest or penalty due from the taxable person under this act upto the time of the partition, whether such tax, interest or penalty has been determined before partition but has remained unpaid or is determined after the partition.

- Save as otherwise provided in the Insolvency and bankruptcy Code 2016, where a taxable person, liable to pay, tax, interest or penalty under this act, is a firm, and the firm is dissolved, then, every person who was a partner shall, jointly and severally, be liable to pay tax, interest or penalty due from the firm under this act upto the time of dissolution, whether such tax, interest or penalty has been determined before the dissolution, but has remained unpaid or is determined after dissolution.

- Save as otherwise provided in the Insolvency and bankruptcy Code 2016, where a taxable person, liable to pay tax, interest or penalty under this act, –

a) is the guardian of a ward on whose behalf the business is carried on by the guardian ; or

b) is a trustee who carries on the business under a trust for a beneficiary,

then, if the guardianship or trust is terminated, the ward or the beneficiary shall be, liable to pay tax, interest or penalty due from the taxable person upto the time of termination of the guardianship or trust, whether such tax, interest or penalty has been determined before the termination of guardianship or trust but has remained unpaid or is determined thereafter.

Analysis: Where a proprietor fails to pay any tax, interest or penalty and his legal representative carries on such business after his death, then such legal representative shall be held liable. In case the business is discontinued, whether before or after the proprietor’s death, such amount payable shall be recovered out of the estate. Where the property of a HUF or AOP is partitioned among its various members, then they shall be liable to pay the pending tax till the date of partition. Where a firm fails to pay tax and is dissolved, then its partners shall be liable to pay the pending tax till the date of dissolution. Where the guardianship or trust is terminated, then the ward or beneficiary shall be liable to pay the pending tax upto the time of termination of the guardianship or trust.

Section 94: Liability in other cases

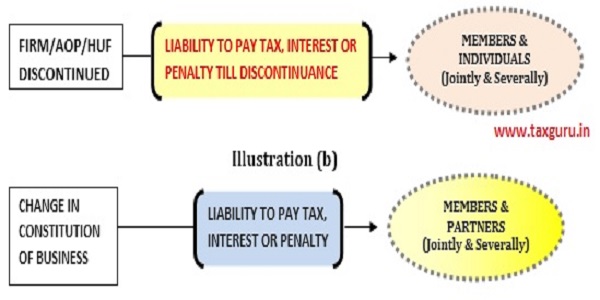

- Where a taxable person is a firm or an association of persons or a Hindu Undivided family and such firm, association or family has discontinued business –

a) the tax, interest or penalty payable under this act by such firm, association or family upto the date of such discontinuance may be determined as if no such discontinuance has taken place; and

b) every person who, at the time of such discontinuance, was a partner of such firm, or a member of such association or family, shall notwithstanding such discontinuance, jointly and severally, be liable to tax and interest determined and penalty imposed and payable by such firm, association or family, whether such tax and interest has been determined or penalty imposed prior to or after such discontinuance and subject as aforesaid, the provision of this act shall, so far as may be, apply as if every such person or Partner or member were himself a taxable person.

- Where a change has occurred in the constitution of a firm or an association of person, the partners of the firms or members of association, as it existed before and as it exists after the reconstitution shall, without prejudice to the provisions of section 90, jointly and severally, be liable to pay tax, interest or penalty due from such firm or an association for any period before its reconstitution.

- The provision of sub section (1) shall, so far as may be, apply where a taxable person, being a firm or AOP is dissolved or where the taxable person, being a HUF, has effected partition with respect to the business carried on by it and accordingly references in that sub section to discontinuance shall be construed as reference to dissolution or to partition.

Analysis: Where a firm, AOP, HUF has discontinued its business fails to pay tax, interest or penalty, such entity shall be liable to pay the pending amount upto the date of such discontinuance. Every partner or family member of such entity shall be jointly or severally liable to pay tax imposed before or after such discontinuance.

*****

Author – CA PRAVEEN KUMAR SURANA, PRAVEEN SURANA & ASSOCIATES, Chartered Accountant in Practice from Kolkata can be contacted at psurana.associates@gmail.com.

{kind=link}

{kind=link}