Changes will impact several M&A transactions, including internal restructuring by companies which were signed since April 2020.

Tax computation will not include goodwill and the cost of acquisition to be regarded for any self-generated goodwill be considered as zero

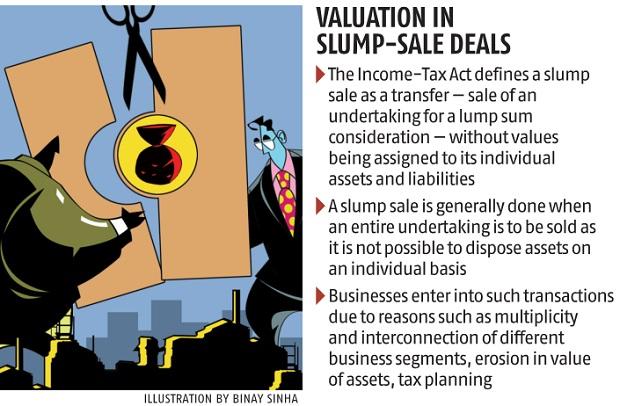

The mergers and acquisitions (M&As) signed in the current financial year (2020-21, or FY21) will have to take into account the amended Finance Bill which states that the net worth for computation of capital gains tax on slump sales will have to be on the full market value of the asset and not the consideration received by the buyer.

The tax computation will not include goodwill. The cost of acquisition to be regarded for any self-generated goodwill will be considered zero. This will lead to increased litigation, with companies objecting to the fair-market value formula.

The new norms will impact several M&A transactions, including internal restructuring by companies signed since April 1, 2020.

In a slump-sale transaction, the seller gets a lump sum amount without any value assigned to its assets or liabilities. While calculating the tax, the department will now take into account the fair market value of the asset if it is higher than the consideration received by the buyer via the slump-sale route.

ALSO READ: Supreme Court to deliver judgement in Tata-Mistry case on Friday

One of the largest slump-sale transactions in FY21 was signed between Future Retail and Reliance Retail after the former merged all its companies into a group company and sold the retail business to Reliance for Rs 24,713 crore.

Future’s merged entity is to hold a few smaller businesses — like stakes in the insurance business. A Future group official, however, said the new norm will not impact the tax treatment for its deal with Reliance Industries since the business was sold at a loss and there are no capital gains for Future Group. Tax experts said the business transfer or slump-sale transactions can be broadly classified as external transactions i.e., sale to a third party or internal (for example, dropping down the business into a wholly owned subsidiary for sale later or getting an equity partner).

ALSO READ: M&A pick-up: Feb numbers top current fiscal with 44 deals worth $4 bn

“Insofar as external transactions are concerned, no one will want to sell the business lower than the fair-market value. This is antithetical to the ease of doing business. For internal restructuring, this should not apply at all, given there is no tax avoidance intent,” said Ketal Dalal, managing director of Katalyst Advisors.

“The provision is effective from March 31 and is retrospective, but unfortunately brought in a year when the whole world was (and still is) struggling with a pandemic, the likes of which no one has seen,” he added.

Normally, M&A transactions are signed at a value which the buyer and seller consider fair. “It is not reasonable to have an approach that there is an undervaluation in all slump-sale deals. Besides, there are so many checks and balances. It does not make commercial sense for either party. In the rare instance where there could be undervaluation, one suspects that, in the larger context, the values could be very small. To put such outlier provisions in the law is not in the right direction,” he added.

There are several cases already pending in the courts, apart from an appeal in the Supreme Court. The new norm may hit M&As in the coming months, said tax lawyers.