Clipped from: https://economictimes.indiatimes.com/mf/mf-news/taxman-puts-fund-houses-hnis-on-watch-over-past-dividend-stripping/articleshow/81676349.cmsSynopsis

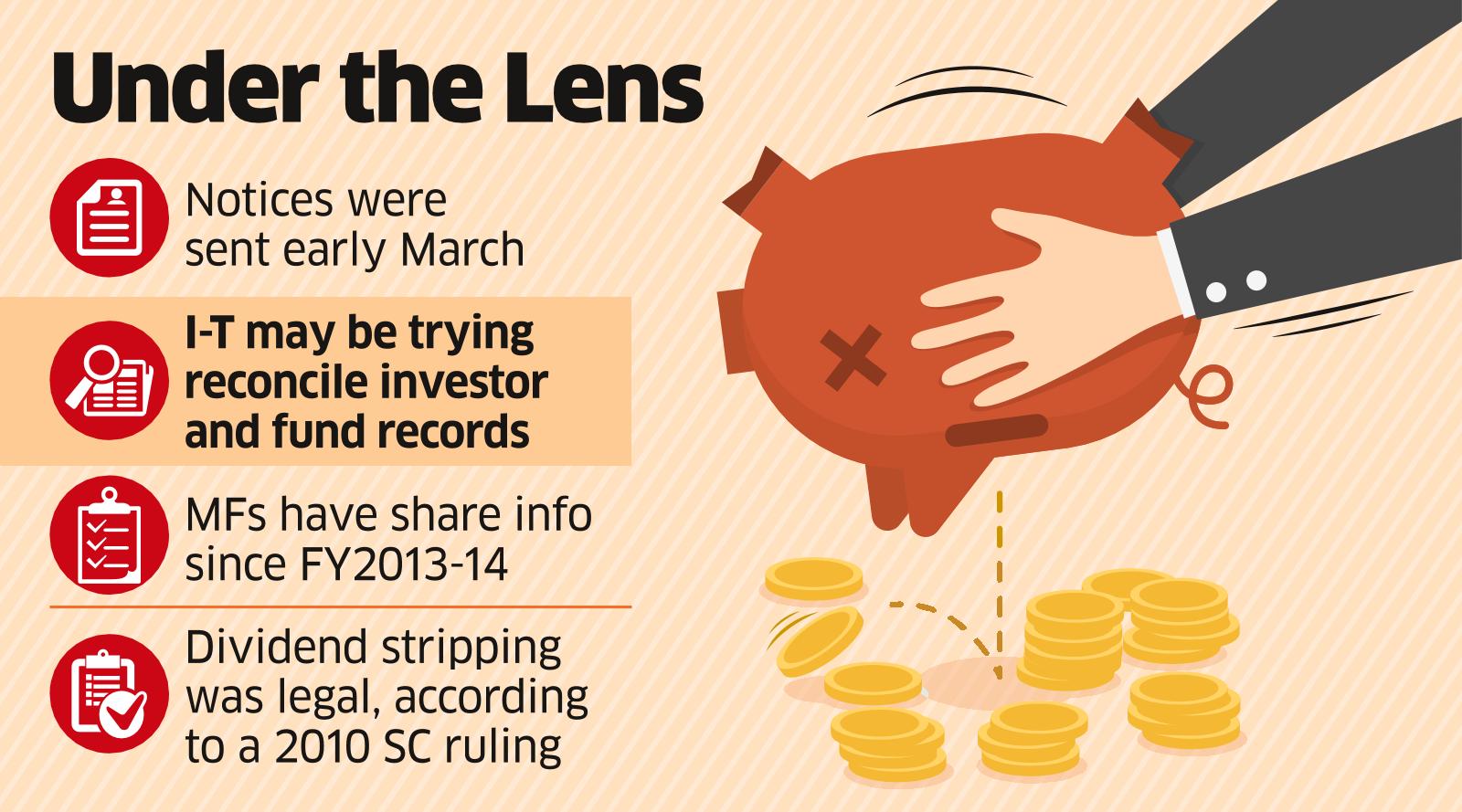

Sends notices asking for information on payouts and redemptions during FY14 to FY20 period

Old deeds have come back to irk some of the mutual fund (MF) houses and their wealthy clients.

The income tax department is raking up the sharp practices of the past like ‘dividend stripping’ which let many high net worth individual (HNI) investors in MFs escape tax.

Earlier this month, the tax office asked at least three large fund houses to share information on dividends paid, dividend dates and redemption amounts from FY14 to FY20, according to three persons aware of the development.

Under dividend stripping, which was rampant at one point, MFs declared a huge dividend — which was then tax-free in the hands of the investors — causing a fall in a scheme’s net asset value (NAV), and paving the way for many investors to redeem their holdings at a capital loss that was used to reduce tax by offsetting capital gains on other investments.

The game died out as the government and subsequently, the capital markets regulator changed the tax laws and rules. The notices to the fund houses were sent under Section 133(6) of the Income Tax Act which allows tax authorities to obtain information that may be used in an inquiry.

“The information from MFs was probably sought after tax officials found extensive tax planning and booking of capital losses in earlier years. However, the department may also question if MFs had distributed dividends from the principal amounts that investors had put in and not out of their earnings. Technically, that was possible. So, if the department is probing whether the fund was an accommodating party to facilitate tax evasion, it may not be easy to establish,” a person familiar with the matter told ET.

The government plugged the loophole in the FY21 budget, making dividends taxable in the hands of investors. Till then, the dividend payer paid the taxes. This has made dividend stripping unsuitable for reducing tax outgo.

Mutual funds typically used a small-sized scheme to facilitate the process of dividend stripping. First, the scheme would create a corpus proportionate to the money it would receive from investors and the dividend it has to pay, following which HNIs would bring the money into the scheme.

The investments had to be brought in three months before the dividend payment and had to be held nine months after the date for them to be eligible for taxation benefits. Once the dividend is paid and the scheme’s NAV falls, the losses from the drop in the fund’s value would be used to set off gains elsewhere.

Dividend stripping was not illegal but the tax department frowned upon this practice because it caused big losses to the government. “As of now, it’s an information-gathering exercise where the department may be trying to reconcile the records of MFs with that of the investors who did not compute the tax properly,” said an industry source.

Responding to ET’s email query, fund industry body AMFI said, “AMFI is not aware of this matter and hence we are unable to comment on the same.”

It is unclear at this stage as to how the tax department would pursue its line of inquiry. Despite media reports and reservations voiced by market observers, activities like dividend and bonus stripping continued for a long time. In fact, in July 2010, the Supreme Court dismissed the tax department’s petition against a Bombay HC ruling that the loss incurred by assessees in dividend stripping transactions cannot be disallowed on the ground that it was tax planning.

In October 2020, Sebi directed MFs to ensure that whenever ‘distributable surplus’ is given out, a ‘clear segregation’ between income distribution (NAV appreciation) and capital distribution (equalisation reserve) is made in the consolidated accounts given to investors. By then, changes in the law had made dividend stripping unattractive.