SynopsisThe link between TDH and DHFL’s insurance business follows a complex trail of transactions that show that DHFL had funded entities that in turn had financed the acquisition when DHFL divested its stake in the insurer resulting in allegations of round tripping of funds.

TDH Reality LLP, a little known Kanpur-based company with a capital of just about ₹1 lakh, is, according to papers filed with the court, acted as an intermediary that ended up having the rights over the insurance arm of the DHFL, the first non-banking finance company to face insolvency and bankruptcy proceedings.

The link between TDH and DHFL’s insurance business follows a complex trail of transactions that show that DHFL had funded entities that in turn had financed the acquisition when DHFL divested its stake in the insurer resulting in allegations of round tripping of funds.

Thus, DHFL did not gain from the transfer of the insurance business. TDH has told the court that the insurance arm cannot be sold again as it already has claim over it.

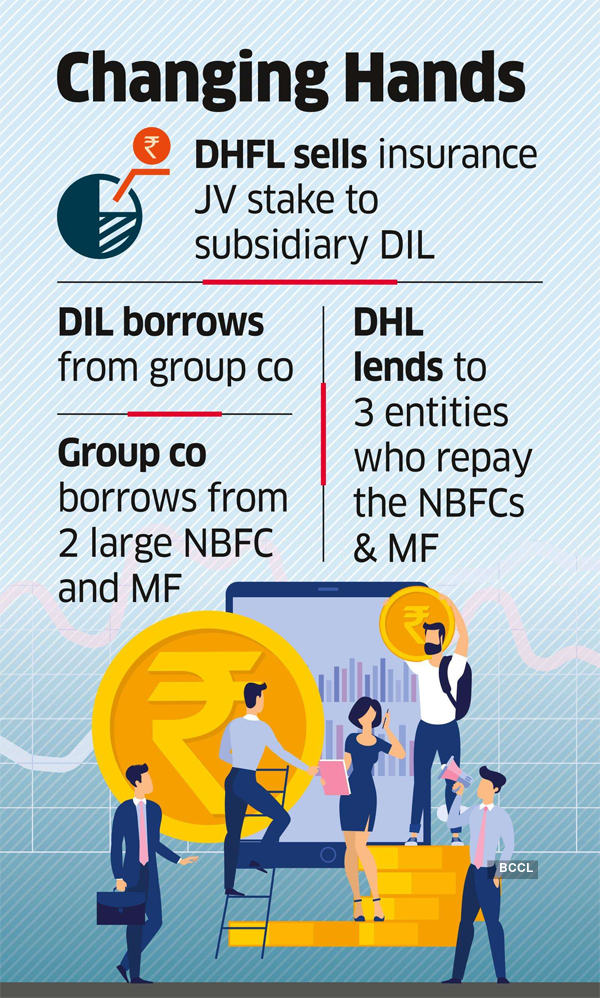

A few years after acquiring control by buying out DLF’s stake in DLF Pramerica Life Insurance in 2013, DHFL decided to divest from the business. The transaction involved transferring the stake to DHFL Investment Company (DIL), a wholly owned subsidiary. The multiple deals that followed were aimed at arranging finance for DIL to buy out DHFL’s stake.

It began with DIL receiving ₹1,900 crore against sale of compulsory convertible debentures (CCDs) to WGC, an entity controlled by the DHFL promoters Wadhawans. CCDs, which are quasi-debt, had put option, which when exercised by the investor required DHFL to pay back the money. This meant that although DHFL recieved ₹1,900 crores but at the very same time had a continegent liability of the put option. WCG, however, did not pay from its own funds. In turn it issued non-convertible debentures (NCDs) to three top financial institutions — Aditya Birla Finance, Birla Sunlife, and Franklin Templeton — to raise funds. The story takes a different turn after this.

Anyone holding the NCDs would eventually have a right over the insurance company: since the CCDs were the underlying securities to the NCDs, a default on NCDs would allow investors to have control over the CCDs and the put option foisted the liability on DHFL.

But this did not happen when the original NCD holders wanted an exit from this deal. Instead, DHFL, the main company which divested its insurance business, lent money (as inter-corporate deposits or ICDs) to three entities — West End, Advent and Abhinandan — which bought over the NCDs from the two Birla companies.

Subsequently, two of these entities to whom ICDs were given , West End and Advent assigned the rights under the NCDs to TDH Realty which also took over the liability arising from ICDs owed to DHFL. This web of deals eventually led to a situation where TDH has borrowing due to DHFL in form of ICDs (on its liability side) while it holds debt instruments that gives it the right over the insurance company where DIL, a DHFL subsidiary, owns 50% stake.

This was a decision, according to TDH’s submission to the court, “taken purely for commercial reasons for obtaining profits on account of the following: (a) the NCDs bore yield calculated at 9.95% per annum where as the loans by way of ICDs given by DHFL in respect of which the repayment liabilities were taken over by the applicant carried with it a significantly lower interest being 8.15% per annum. (b) The NCDs were AAA rated (c) NCDs were backed by an expressed guarantee given by DHFL by way of option agreement dated 30.03.2017 which clearly and expressly provided that DHFL would purchase the CCDs at the put option price when called upon to do so.”

No other connections have been established till now between the DHFL promoters and West End, Advent, and Abhinandan, and TDH.

The TDH application before the National Company Law Tribunal (NCLT) comes at a time the court is hearing resolution plan for the takeover of DHFL by the Piramal group after a fierce bidding war.

If TDH eventually wins the case, it may invoke the put option and DHFL is likely to ask TDH to pay back the ICD. But legal circles think that untangling the insurance piece could see more court cases. DHFL’s outstanding borrowings to different set of creditors — banks, funds, and retail and corporate investors — is around ₹87,000 crore.