Synopsis–As the economy limps back to normalcy, demand recovery still remains nascent and vulnerable. While optimism seems high and the stock market bulls run amok, investors should be mindful of the pitfalls along the way. Markets can stay overheated for a long time.

The March 2020 stock market rout seems a distant memory. After a nearly 40% cut in frontline indices, the bulls are back with a vengeance. After gaining more than 100% since last year’s lows, the Sensex and Nifty have hit record highs. A gradual phasing out of lockdown restrictions, resumption in business activity and rolling out of vaccines have sent stock prices soaring. The government’s booster shot in the form of an expansionary Budget only added fuel to the fire.

Consequently, valuations have got stretched. Yet, there are voices suggesting this party has only begun. Interest rates are at historical lows, providing an ideal platform for earnings to pick up. Liquidity is flowing like a river in spate. India’s leading companies look set to bounce from historical lows in corporate profits. While optimism seems high, there are several questions that can’t be ignored. Is the recovery truly entrenched? What rate of earnings growth is built into prices? What happens if earnings do not catch up as expected? Are traditional valuation multiples painting a distorted picture?

Demand recovery is nascent and vulnerable

With a modest 0.4% GDP growth, the economy broke out of recession in the October-December quarter, following two successive quarters of growth contraction. With the economy opening up in the festive season, pent-up demand got unleashed. Sales have since continued to rebound at a faster pace than costs, resulting in broad-based earnings beat. This is the third consecutive quarter when more companies beat estimates than missed them. Cyclical sectors are driving incremental earnings.

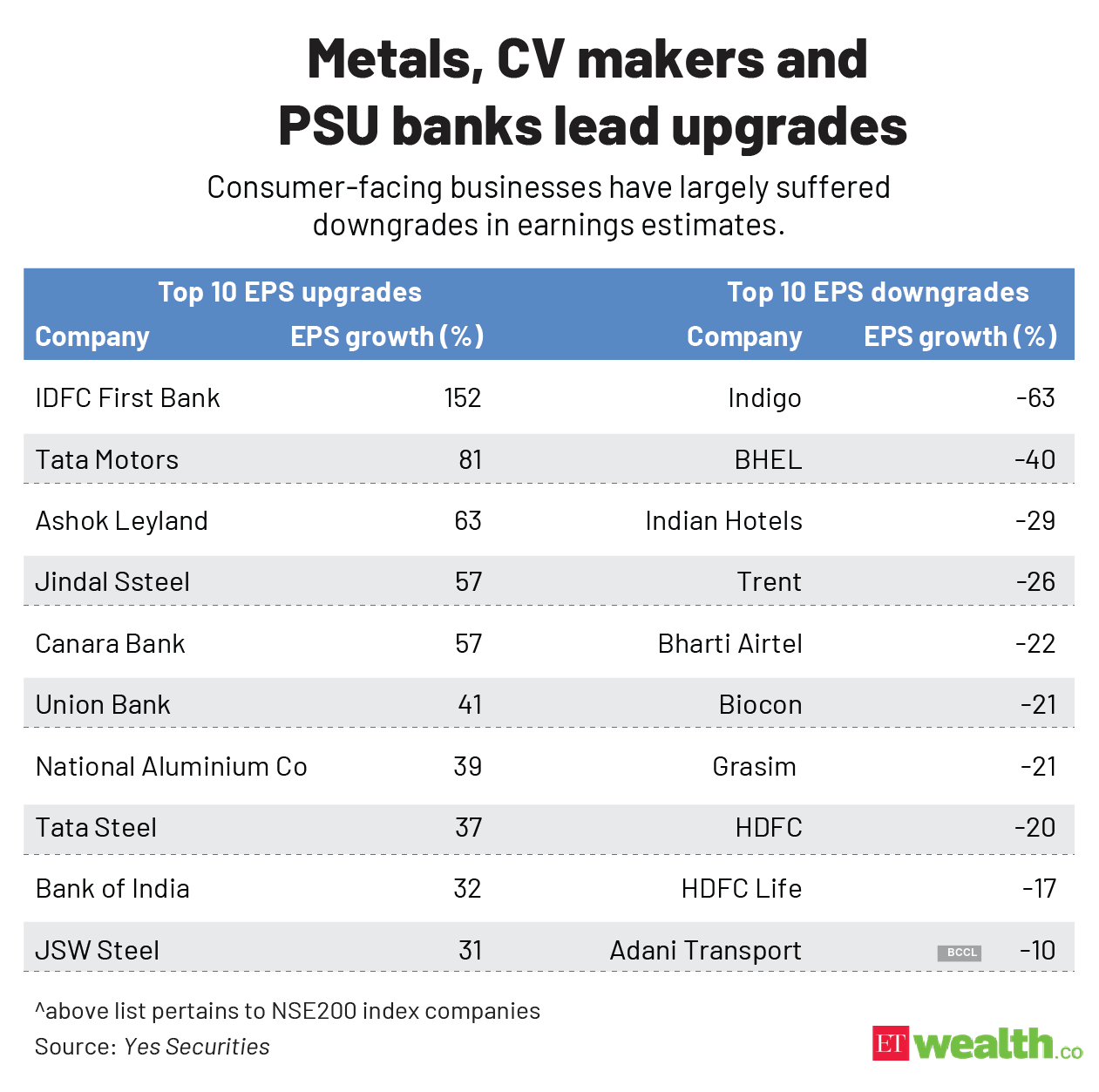

After the strong earnings show in the December quarter, consensus estimates for corporate earnings saw another round of upgrades—on top of healthy upside revision during the previous quarter. A sequential earnings upgrade was last observed during the second quarter of 2014-15. With an upgrade to downgrade ratio of 7:2, this has been a blockbuster earnings season. Further, this upgrade is not confined to 2021-22, analysts are anticipating higher earnings for 2022-23 as well.

The concern is that bulk of this recovery has been in the form of pent-up demand coming through. Question now is whether the economy can transition from pent-up demand to sustainable demand. Recent evidence based on high frequency numbers indicates that recovery is still a work in progress. The Care Ratings Economic Comeback Meter shows that the economy has been “on a comeback path” for six months. Select parameters have seen a gradual but sustained improvement in this period. However, it is still far from a comeback. After the broad-based improvement seen in December 2020, several early available economic indicators showed a loss of momentum in January 2021 relative to the previous month. As the favourable base effect fades, many indicators will remain subdued.

While the economy may have formally come out of recession, a part of this “growth” can be attributed to downward revision in previous year’s figures. Further, despite the expansion in the third quarter, the GDP for 2020-21 is projected to contract by 8%—more than the 7.7% estimated earlier. This implies that recovery is not happening as fast as expected. CARE Ratings says in its report that the continuation of momentum should help 2021-22 GDP growth to move towards 10.5%. “However, sustainability needs to be monitored, especially as the recovery appears to be led by capital and profits, and not improvement in labour and wages,” the report notes. Moreover, economic recovery needs to broaden further to more sectors for it to sustain, insist analysts. Still, the focus on capex (which has higher multiplier effect on demand), pro-growth policies together with low interest rates and ample liquidity set the stage for a favourable demand environment. “The environment is conducive for driving the ‘invisible hand’ which could boost aggregate demand from private sector and households sustainably beyond the pent-up demand seen in October-December,” suggest analysts at ICICI Securities.

What can derail juggernaut

Despite the positive momentum in economic recovery, some dark clouds hover. The fledgling recovery environment remains vulnerable to certain shocks. “A second Covid wave in India, continued supply disruptions and rise in global rates pose risks to the nascent economic recovery,” points out Edelweiss Securities.

Of late, stock markets have been left spooked by the rise in bond yields in the US. The spike in US bond yields from 0.5% to 1.5% is owing to expectations of rising inflation in the country, on the back of faster than expected recovery in the US economy. Rising yields in the US beyond 2-3% can potentially lead to a reversal in capital flows away from equities, which is what unnerves equity markets globally. Rusmik Oza, Executive VP and Head of Fundamental Research at Kotak Securities, observes, “As we go into the calendar year we could witness further rise in bond yield which will lead to moderation in equity valuations thereby suppressing returns from a short-to-medium term.”

However, experts maintain that further rise in bond yields may not necessarily derail the stock markets. The underlying reasons for uptick in bond yield are more relevant than the level of yield, argues Madhavi Arora, Lead Economist, Emkay Global Financial Services. “There should not be too much ado about pace of uptick in yields as long as the reasons behind that are right.” She argues that current yield momentum is owing to cyclical economic acceleration and optimism. Equities as an asset class typically perform better in an environment of ‘rising growth’ and ‘moderate inflation’. For example, despite the rise in Indian bond yields from around 5% to 9% and US yields from 3.5% to 5% from 2003 to 2007 as demand-led inflation picked up, global stock markets including India had their best run as growth kept surprising on the upside.

A glance at similar instances of rising yields in the past provides comfort for a wary equity market. “Our assessment of the last two recession cycles shows an increase in US 10-year rates of at least 100 bps from their recession lows is typical just before or just after the recession ends. Thus, neither the direction nor the magnitude of yield increases is odd,” says Arora. Besides, the last decadal cycle depicts that whenever yields have spiked more than 50bps in a short period of time, stocks have performed well. However, a debilitating environment for stocks is that of rising yields and slowing growth or stagflation. If growth slows down in an inflationary environment, it will mean trouble for equities.

Valuations: Singing same tune

After the sharp uptick in the past few months, most key metrics now point to lofty valuations in the market. The Nifty50 index is now valued at roughly 40 times trailing 12-month earnings, against its two decade average of 20 times. In terms of price-to-book value, the index stands at 4.3 compared to 20-year average of 3.5. India’s market cap to GDP is hovering above 100%—much higher than its average of 77% since 2003. Clearly, all indicators are pointing to overheating in the market. Yet, there are multiple arguments justifying these stock prices and valuations.

Analysts are no longer using 2020-21 earnings estimates as the basis for valuing companies. Earnings estimates are being rolled forward by another year to 2021-22 or even 2022-23 to arrive at current PE multiples. The argument is that earnings for the current financial year have been impaired owing to pandemic-led disruptions. “Valuation multiples cannot be seen in context of current earnings in the wake of the severe disruption in businesses,” insists Kunj Bansal, CIO, Karvy Capital. Analysts are instead turning to 2021-22 and beyond for a return of normalcy in both the economy and corporate profitability. The index valuations relative to estimated forward earnings suddenly appear quite reasonable, with upward revision in estimates for next two years. The Nifty index PE drops from prevailing 40 times on trailing basis to 22 and 20 times respectively, for the next two years. For these valuations to be justified, earnings of Nifty 50 companies have to jump by 20% CAGR by 2022-23. If earnings do not catch up, it will lead to repricing of equities.

All valuation metrics indicate market is expensive

Markets can stay overheated for a long time. While there will be deep corrections along the way, it is difficult to predict when that will happen.

Corporate profit to GDP is another metric that seems to indicate value right now. India Inc’s profitability as a portion of the country’s GDP is currently at multi-year lows, suggesting that earnings will only improve from hereon. But even assuming that is true, experts question how much of this is already factored into prices. “The last time this ratio was so low in 2001-02, index valuations were half of where they are today,” argues Abhishek Singh, AVP – Equities, DSP Mutual Fund.

Another argument is that valuations are justified as interest rates are at historical lows. Conventional wisdom around valuations is being tested in the face of near-zero or sub-zero interest rates worldwide. “While the equity markets are currently trading at higher than historical averages on conventional valuation metrics, strong global liquidity and a low cost of capital environment in India as well as globally, places equity as a relatively better asset class in the near to medium term,” insists Ravi Menon, CEO, HSBC Global Asset Management. The premise is that if interest rates are low, the discounted value of future cash flows—a common approach to value stocks—is that much higher. So today’s valuations are not out of whack. This argument seems to have that familiar ring of “this time it’s different” to it, say critics. “Most advocates of this argument assume future cash flows remain constant as interest rates fall. But earnings are correlated to inflation, which in turn is correlated with interest rates. Lower inflation means lower earnings growth,” argues Singh.

Here is another widely held belief these days: you will never make money if you worry about valuations. Quality stocks deserve to be rewarded with hefty premiums, some argue. If you are thinking on the same lines, watch out. “Think of the most extreme bubbles in history. You will find the same sentiments echoed in each of them,” remarks Singh. The infamous US-based Nifty Fifty basket in the 1970s is a classic example. Market darlings like Coca Cola, Xerox, Eastman Kodak, Gillette, Polaroid and Walt Disney, among others, ruled the charts in that era, commanding PE multiples in excess of 60-70. When the bubble burst, these names cracked by 60-90%. It took decades for this basket to recover lost value.

Current valuations are nowhere close to such frothy levels—at least not in broader markets. Yet, the risk-reward is not in favour of equities. “Nifty valuations are not inexpensive any more and demand consistent earnings delivery,” say analysts at Motilal Oswal Securities. Even if the stock market is not in an extreme bubble, it is definitely in a trance. Investors would do well to be cautious. “I don’t think we are in a bubble but I do believe sentiments and valuations are high while fundamentals are recovering. We might have factored in possible improvements in economic prospects but we are ignoring downside risks,” Singh observes.

Even so, markets can stay overheated for a very long time. While there will be an inevitable deep correction along the way, there is no way to tell when that will happen. What you can expect is a fall every now and then. An analysis by FundsIndia looked at data as far back as 40 years ago to check maximum declines recorded each and every year— fall from the highest index value to the lowest index value during the year. Here is what was found: A 10-20% temporary fall is a given every year. A 20-30% dip can be expected every three to five years. A steep correction in the range of 30-60% can be expected every seven to 10 years. Investors should build in expectations accordingly and be prepared to live through these corrections, notes Arun Kumar, Head-Research, FundsIndia.

For now, experts maintain there are select pockets of opportunity still available for investors. HDFC Securities reckons that economy-facing sectors like banks, cement, infrastructure, real estate, utilities and gas still have room for re-rating while IT and pharma look fairly valued with earnings driven upsides. Consumer staples and discretionary face PE de-rating risks, given stretched valuations. Oza also favours an accumulation strategy in economy-driven sectors on every decline. “Few sectors and pockets that we can visualise can make money for investors given their past underperformance and potential recovery are banks, capital goods, construction, engineering, oil and gas, cement, real estate and metals.”

(Graphics by Sadhana Saxena/ET Prime)