Clipped from: https://economictimes.indiatimes.com/industry/banking/finance/banking/break-even-year-for-bleeding-psu-banks/articleshow/79986384.cmsSynopsis

Given this setting, it may seem highly incongruous to expect NPAs in Indian banks to bottom out in the fourth quarter of 2020-21. Yet, this is what is likely to happen. It now appears that not only have banks dodged an explosion of bad loans, but they also solved some historical problems.

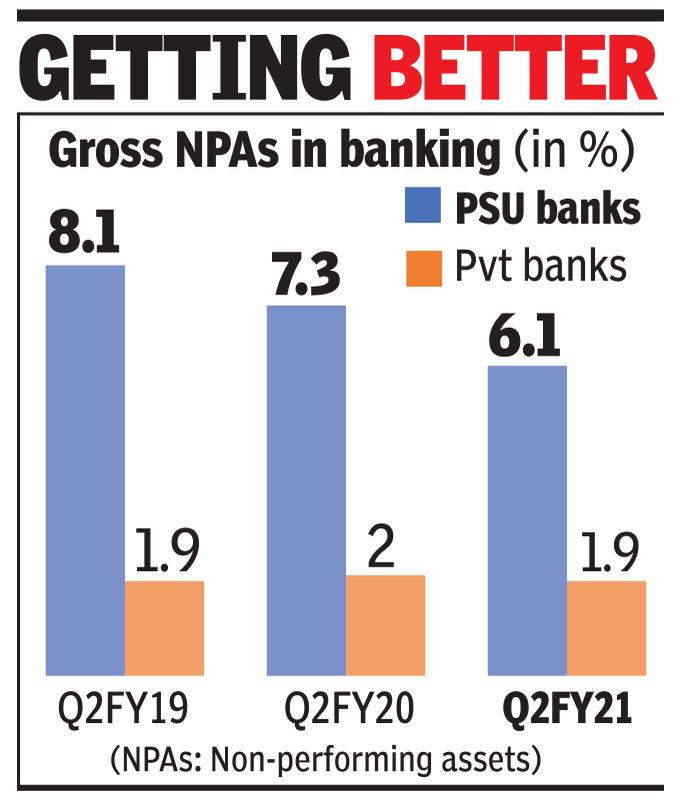

(This story originally appeared inon Dec 28, 2020)NEW DELHI: The economy has shrunk 15.7% in the first half, jobs have been lost, incomes have contracted and uncertainty hangs over high-contact services with the survival of many in doubt. India has the second-highest ratio of net non-performing assets (NPAs) among the G-20 nations. And this is expected to go up when the Supreme Court stay on NPA classification gets lifted.

Given this setting, it may seem highly incongruous to expect NPAs in Indian banks to bottom out in the fourth quarter of 2020-21. Yet, this is what is likely to happen. It now appears that not only have banks dodged an explosion of bad loans, but they also solved some historical problems. For instance, NBFCs were facing a huge credit crunch in March and there were fears that they might default. The targeted long-term repo operations and other schemes enabled them to refinance loans that were coming up for repayment in the current fiscal.

While none of the RBI or government relief measures were available for companies that had defaulted, these bad loans have been addressed through provisions. “After six years of losses, FY2021-22 may be the break-even year for public sector banks. This year, there is a possibility that they will make a loss if the stress will materialise according to our estimates,” said Anil Gupta, Icra VP and sector head.

According to him, private banks will bounce back next year (in FY22) to pre-Covid levels in terms of return on assets because they have already made the required provisions. “We expect that net NPAs will rise to 3.1% in March 2021 before coming down to 2.5% in March 2022,” Gupta added.

Banks have already made significant provisions towards stressed loans this year and in the second half private banks are expected to set aside an additional Rs 60,000 crore, while public sector banks will need to keep an additional Rs 1 lakh crore, which will wipe out most of their earnings this year. Despite such heavy-duty provisions, they should be able to bounce back in FY22.

Thanks to buoyant capital markets, banks have raised close to Rs 70,000 crore of equity capital and this could go up to Rs 1 lakh crore. This capital is enough to provide for their stock of bad loans. Private banks have already set aside 2.4% of their advances in the form of provisions. As against the full-year provisioning requirement, estimated at 3% of their advances by ICRA, private banks have already got total provisions of 2.4% in the first half.

The conventional response to an economic crisis in the past has been to give defaulters more time to repay. This time, the RBI’s response has been different. The central bank flooded lenders with liquidity, bringing down interest rates and provide borrowers with a moratorium to enable them to survive the lockdown.

While the RBI did not directly lend money to NBFCs and corporates, it nudged them to do so by refinancing loans at very cheap rates. The government took on credit risk through various guarantee schemes. For now, the measures seem to be working.