Synopsis–Crude steel production in November grew 6.6 per cent year-on-year driven by an 8 per cent growth in China and 5.5 per cent jump in Europe.

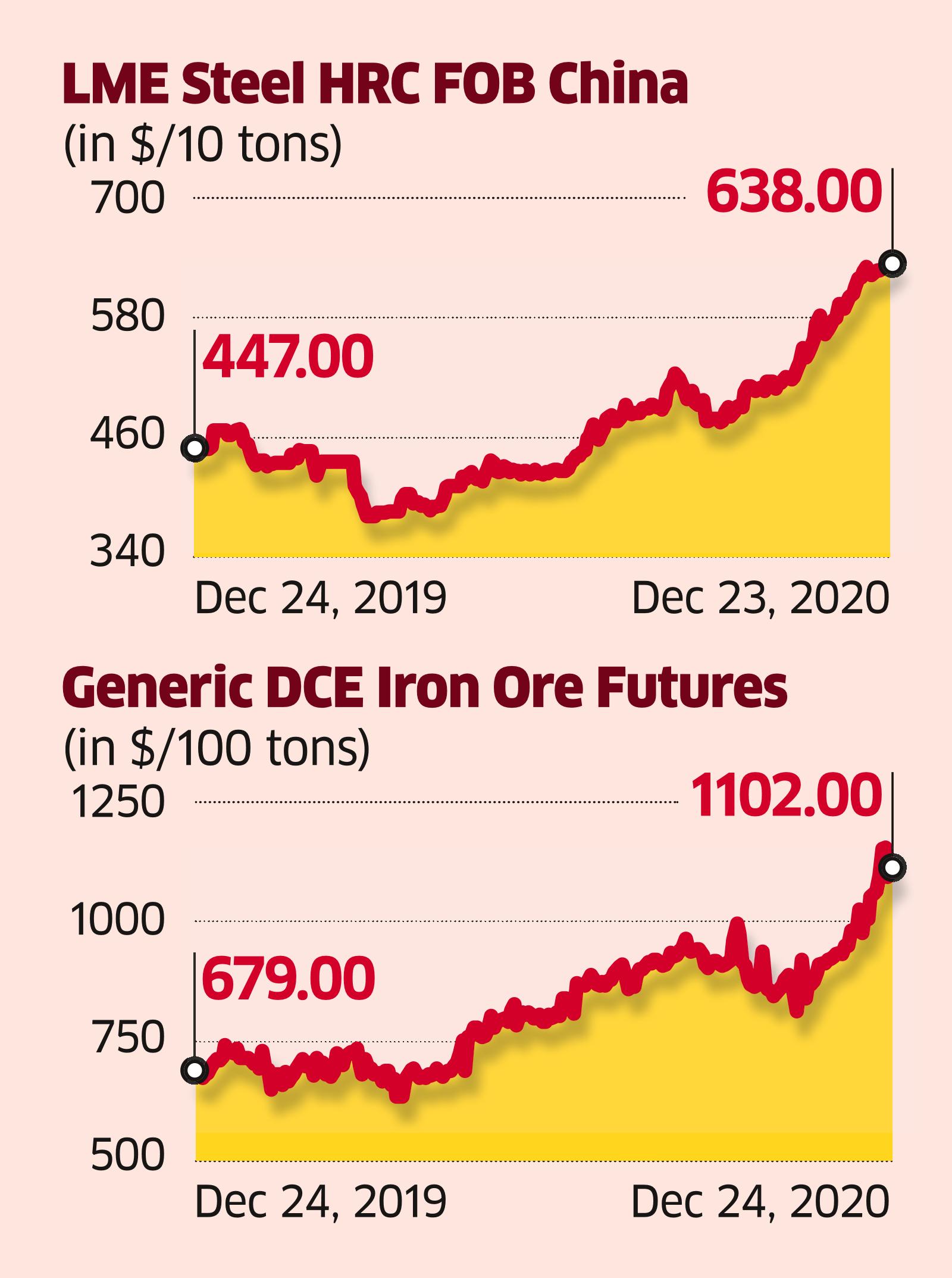

ET Intelligence Group: Steel prices in China and the US are at 12-year highs while in most other markets, including India, they have touched an eight-year high. While this should benefit steelmakers, a sharp jump in prices of iron ore, a major raw material, may spoil the party. Under such conditions, steel companies with captive iron ore mines stand to gain the most. Among the listed steel companies on Indian bourses, Tata Steel looks better placed.

Crude steel production in November grew 6.6 per cent year-on-year driven by an 8 per cent growth in China and 5.5 per cent jump in Europe. This has increased the lead time or delivery time for finished steel creating shortage of the alloy.

In addition, iron ore prices have shot up by 25 per cent, much faster than the 12.5 per cent rise in the domestic steel prices over the past month. This is due to the shutting down of mines by Brazil’s mining major Vale due to landslides. Vale is the second-largest iron ore producer, accounting for nearly 20 per cent of global supply. The miner has lowered the production guidance for 2020 and 2021, indicating that the supply shortfall is likely to stay for a few more months.

Domestic steel makers have raised prices four times over the past month. Sector experts believe there is still some room left since the domestic prices are at a 5 per cent discount to the imported prices.

Analysts expect Tata Steel’s operating profit before depreciation and amortisation (EBITDA) to grow by 34 per cent year-on-year to ₹23,500 crore in the second half of the current fiscal. In the September quarter, its EBITDA had increased by 60 per cent to ₹6,110 crore following negligible profit in the previous quarter. Higher earnings are likely to accelerate the deleveraging process, which has been an overhang on the stock. It reduced the net debt by 8 per cent year-on-year to ₹96,500 crore in the September quarter.

Share the joy of reading! Gift this story to your friends & peers with a personalized message. Gift Now