The escalation of conflict in the Middle East has pushed global oil prices higher, exposing a familiar fault line in India’s external position. Despite robust domestic growth, the rupee has slipped to record lows and equity markets have turned volatile. Why has strong growth and contained inflation not insulated the currency? In the near term, oil and risk premia dominate pricing when patient capital is scarce.

This is a flow story overwhelming a stock story: war-driven energy shocks and a stronger dollar have collided with thinner, more flighty capital inflows — pressures that overwhelm fundamentals in the short run and take years to adjust. Let’s understand this better.

The disconnect

On paper, India’s macro story is reassuring: growth projected at 7.4 per cent this fiscal, inflation relatively contained, reserves near $701.4 billion, a current account deficit (CAD) of about 0.8 per cent of GDP, and resilient services exports and remittances. Yet the rupee fell by more than 5 per cent last year and has hovered near recent lows. The proximate drivers are clear. As a large oil importer, India’s dollar demand jumps when crude spikes, widening the trade deficit and squeezing corporate margins; at the same time, a stronger dollar tightens global financial conditions.

Ordinarily, a modest CAD is easily financed, but in 2025 foreign portfolio investors pulled back and net FDI softened as profit repatriation and outbound investment rose. That shift changed the market’s risk calculus. With less patient capital, the rupee became more sensitive to shifts in risk appetite. As oil buyers needed more dollars just as investors sought safety, the rupee took a hit from both sides.

Rupee dynamics

Why couldn’t fundamentals defend it quickly? In the short run, risk and oil premia price the currency. In the long run, fair value anchors it.

On that front, we tried understanding the rupee dynamics, and purchasing power parity (PPP) offers one such long-run compass. It indicates where the currency tends to settle once shocks fade. From that perspective, our pre-shock estimate placed the rupee roughly 18 per cent below PPP fair value (also referred to as “equilibrium” in economic literature).

We computed equilibrium using monthly real exchange rate (RER) data for more than three decades, following PPP theory that RER exhibit a mean-reverting behaviour.

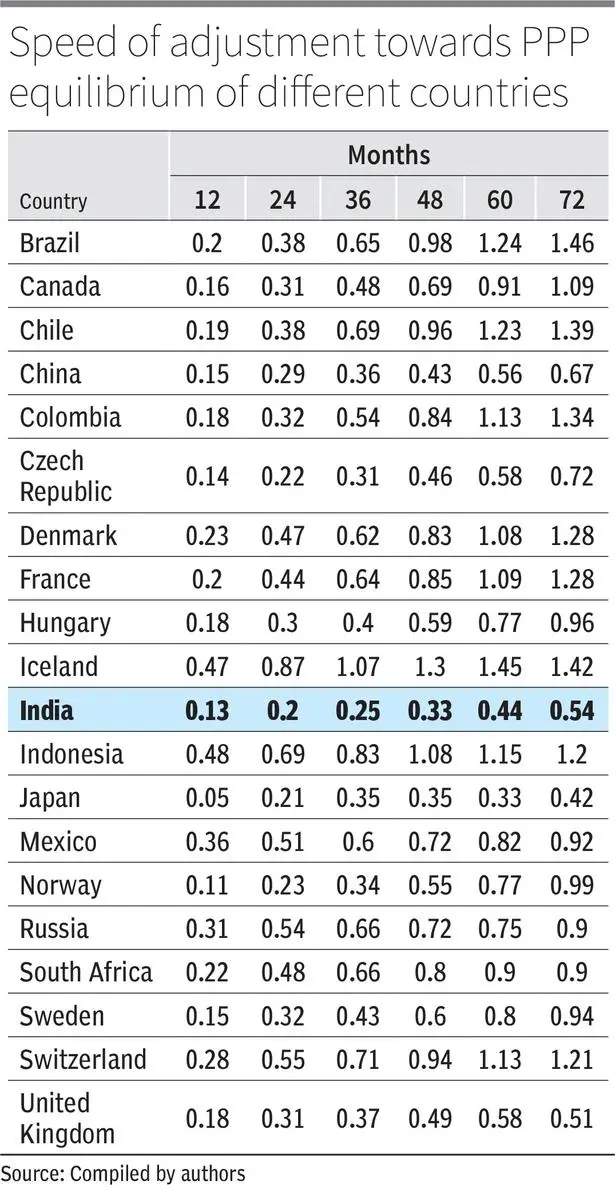

The key nuance is speed: India’s adjustment towards PPP is slow (as shown in the Figure), with a half-life of more than five years, meaning only half of any misalignment typically closes over that horizon.

For instance, in one year, only 13 per cent of the adjustment towards equilibrium is completed; in three years, only 25 per cent; and in five years, just 44 per cent.

Several emerging peers, such as Brazil or Indonesia, appear to adjust faster.

Also, we observed that these adjustments are also uneven: when the currency is far from equilibrium, corrections often arrive abruptly during risk-off episodes and outflows. Put simply, even when fundamentals are sound, the path back to equilibrium is long and bumpy — too slow to offset a sudden oil-and-dollar shock. This explains the current dynamics.

The transmission

Because India imports most of its crude, pricier oil raises the import bill before quantities adjust, widening the CAD and pressuring the rupee. Some of the hit is cushioned by the service surplus and remittances, as well as heading and pricing policies that delay pass-through. Over time, higher prices can curb demand, induce efficiency and alter the terms of trade, gradually narrowing the gap.

Multi-country evidence suggests that for oil importers, a 1 per cent real oil price shock — that is, a 1 per cent increase in the oil price after adjusting for inflation using the US consumer price index — can worsen the current account balance (CAB) by up to 0.08 percentage points (pp) of GDP over five years, while improving oil exporters’ balances by up to 0.9pp in emerging markets (World Bank, 2023). For India, a sustained 10 per cent real increase in oil could translate into roughly 0.8pp of GDP deterioration in the CAB over five years, and a sustained 20 per cent increase about 1.6pp; a persistent 5 per cent increase could imply around 0.4pp. These are cumulative pressures — buffers mute them, but do not eliminate them. Unless capital inflows deepen and diversify, these current-account stresses transmit into the currency during shock years.

Path forward

The rupee’s recent struggles underscore a deeper reality: its trajectory is shaped not only by fundamentals, but by sensitivity to external shocks and capital composition. Durable currency strength requires more than growth and low inflation; it requires resilience in the flow dynamics that matter most during stress.

Near-term shock absorbers include calibrated fuel-tax adjustments to smooth pass-through while protecting fiscal anchors, deploying FX reserves opportunistically to counter disorderly moves rather than to target levels, and strengthening risk management for oil imports through diversified sourcing and prudent hedging.

Medium-term insulation means attracting and retaining higher-quality, “stickier” capital, especially greenfield FDI — by maintaining a stable, predictable policy regime, depending on local-currency financing markets, and reducing policy uncertainty that widens risk premia.

Long-term competitiveness depends on sustainably strengthening the external position by raising export complexity and scale in manufacturing, while accelerating energy security — diversifying crude sources, expanding strategic reserves, speeding the renewables transition, and improving energy efficiency.

Every crisis carries a lesson. This one should prompt policymakers to treat energy security and capital quality as central pillars of external stability, not peripheral goals. By turning a recurring oil-and-flows vulnerability into a managed risk — through better shock absorbers, deeper and steadier inflows, and higher export competitions, India can safeguard the currency through well-calibrated policy responses.

Bhaduri is Professor, and Anand is PhD scholar, Madras School of Economics, Chennai