Listen to this article in summarized format

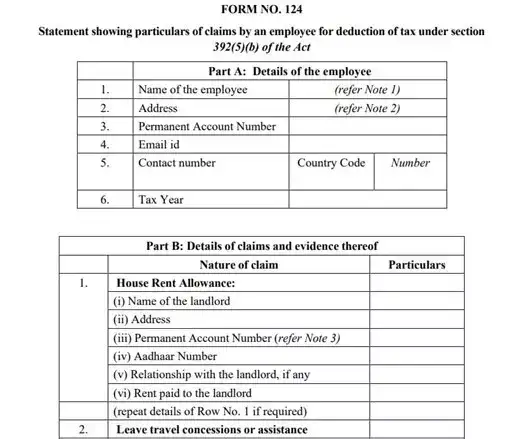

The draft Income Tax Rules, 2026 propose a new disclosure requirement for salaried employees who are claiming House Rent Allowance (HRA). According to these draft income tax rules , taxpayers will need to disclose their relationship with their landlord in Form No. 124 (corresponding to Form No. 12BB) when they pay rent, especially in situations where the landlord is a relative.

Income Tax Guide

Income Tax Union Budget FY 2026-27 LiveIncome Tax Slabs FY 2025-26Income Tax Calculator 2025

Chartered Accountant Suresh Surana mentions that the goal is to enhance transparency and enable the tax authorities to verify the genuineness of rental arrangements.

Surana also points out that while paying rent to close relatives like parents, grandparents, or other family members isn’t outright banned, it does require a closer look at the facts. HRA can only be claimed if the transaction is bona fide and backed by the right paperwork.

Surana says: “However, with such a requirement for declaration under the draft tax rules, taxpayers must explicitly disclose their relationship with the landlord.”

Taxpayers claiming HRA for rent paid to relatives should take the following steps:

- Ensure a genuine landlord-tenant relationship with a clear and written rent agreement.

- Make rent payments through banking channels (bank transfer, cheque, etc.), avoiding cash payments.

- Ensure the landlord declares the rental income in their income-tax return.

- Accurately disclose the relationship with the landlord in the prescribed form while submitting HRA details

Draft tax rules, 2026

How to claim HRA tax benefits

Surana says that it is broadly correct that HRA is unique in the sense that it does not have a fixed monetary ceiling like Section 80C (Rs 1.5 lakh) or Section 80D. However, this does not mean that HRA is unlimited in absolute terms. The exemption is strictly restricted to the least of the following:

(i)The amount of house rent allowance received, or

(ii)50% of salary* in case of employees residing in the four metro-cities (Mumbai, Kolkata, Chennai, New Delhi excluding NCR region – Gurgaon, Noida and Faridabad) and 40% of salary in case of employees residing in other cities, or

(iii) Excess of rent paid over 10% of the salary due for the relevant period.

Therefore, the HRA tax exemption is inherently capped by salary structure, rent paid, and location.

Example – 1 Annual Salary: Rs 18 lakh

- City: Mumbai (Metro)

- Basic Salary: Rs 7,20,000

- Dearness Allowance: Rs 1,80,000

- HRA received: Rs 3,60,000

- Actual rent paid: Rs 4,50,000 per year

The HRA exemption u/s 10(13A) would be least of the following:

| Particulars | Amount (Rs) |

| 1. Actual HRA received | 3,60,000 |

| 2. Rent paid – 10% of salary | 4,50,000 – 90,000 = 3,60,000 |

| 3. 50% of salary (Metro) | 50% × 9,00,000 = 4,50,000 |

The total tax liability would be as follows:

| Particulars | Old Regime | New Regime |

| Gross Salary | 18,00,000 | 18,00,000 |

| Less: Standard Deduction | (50,000) | (75,000) |

| Les: HRA Exemption | (3,60,000) | – |

| Net Salary/ Total Taxable Income | 13,90,000 | 17,25,000 |

| Less: Deduction u/s 80C | (1,50,000) | – |

| Less: Mediclaim Premium u/s 80D | (25,000) | – |

| Taxable Income | 12,15,000 | 17,25,000 |

| Total Tax Liability | 1,84,080 | 1,50,800 |

Example – 2 Annual Salary: Rs 30 lakh

- City: Mumbai (Metro)

- Basic Salary: Rs. 12,00,000

- Dearness Allowance: Rs. 3,00,000

- HRA received: Rs. 6,00,000

- Actual rent paid: Rs. 6,00,000 per year

The HRA exemption amount u/s 10(13A) would be least of the following:

| Particulars | Amount (Rs.) |

| 1. Actual HRA received | 6,00,000 |

| 2. Rent paid – 10% of salary | 6,00,000 – 1,50,000 = 4,50,000 |

| 3. 50% of salary (Metro) | 50% × 15,00,000 = 7,50,000 |

The total tax liability would be as follows:

| Particulars | Old Regime (Rs) | New Regime (Rs) |

| Gross Salary | 30,00,000 | 30,00,000 |

| Less: Standard Deduction | (50,000) | (75,000) |

| Less: HRA Exemption | (4,50,000) | – |

| Net Salary / Total Income | 25,00,000 | 29,25,000 |

| Less: Deduction u/s 80C | (1,50,000) | – |

| Less: Mediclaim u/s 80D | (25,000) | – |

| Taxable Income | 23,25,000 | 29,25,000 |

| Total Tax Liability | 5,30,400 | 4,75,800 |

What precautions to take if an individual is paying rent to parents, grandparents, or even wife and then claiming HRA

Surana points out that the Income-tax Act doesn’t explicitly stop an employee from claiming House Rent Allowance (HRA) exemption where the rent is paid to family members like parents or grandparents, as long as the arrangement is genuine and supported by the right documents.

Surana says: “However, considering the inherent relationship between the parties, the Income-tax Department may, in practice, scrutinise such arrangements more closely to verify the legitimacy and commercial substance of the rent payment.”

According to Surana, the taxpayer needs to show that the arrangement is legitimate and has a valid reason. Plus, they should have documentation like a written rent agreement that clearly states the rent amount, tenure, and property details. Rent should be paid through bank transations instead of cash to create a clear audit trail.

The landlord’s Permanent Account Number (PAN) must be disclosed when annual rent exceeds Rs 1 lakh, and tax deduction at source under Section 194-IB should be complied with, where applicable. Also, the rent received should be offered to tax by the family member under the heads of income: “Income from House Property.”

Surana says that it should be noted that HRA exemption claimed for rent paid to one’s spouse may generally be viewed as lacking commercial substance.

Surana says: “In all cases, the rent amount should be reasonable and consistent with prevailing market rates to avoid allegations of a colourable or tax-driven arrangement.”