Customers should also watch out for sub-limits on room rent and specific treatments

Heart disease

In recent years, heart disease has become one of the leading causes of health insurance claims. Not just the old but even younger people are suffering cardiac ailments.

These diseases impose a heavy financial burden on patients and insurers. According to recent data from Policybazaar, an online portal for the purchase of insurance, heart-related conditions accounted for around 10.5 per cent of all its health insurance claims in 2019-20, with an average claim size of around Rs 4.5 lakh. By 2023-24, their share had climbed to around 19 per cent, with the average claim size reaching Rs 13.5 lakh.

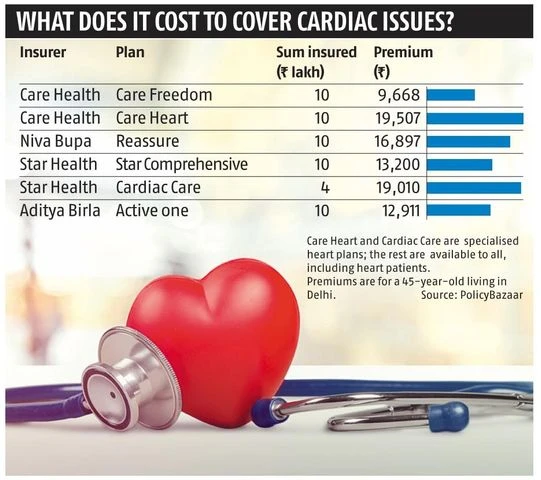

Insurers have responded by offering specialised cardiac plans tailored to the unique needs of cardiac patients.

Pre-existing conditions covered

Specialised cardiac plans cater to those with pre-existing heart issues. “These plans cater to people who have gone through a cardiac event, such as angiography, bypass surgery, and so on,” says Manish Dodeja, head–claims & underwriting, Care Health Insurance.

These plans have a few unique features. “They typically cover expenses related to cardiac devices, such as the pacemaker. Another feature is coverage for the transportation of the heart transplant organ by road or by air,” says Aayush Dubey, co-founder and head of research, Beshak.org.

They also offer many of the features of a standard cover, such as hospitalisation coverage, pre- and post-hospitalisation coverage, no-claim bonus, and automatic recharge.

Free annual check-ups to monitor heart health, diabetes, hypertension, and cholesterol are also available. “This ensures that customers’ heart health gets monitored and key parameters are managed,” says Dodeja.

Lifeline for the ailing

A person who has had a cardiac event or is suffering from a cardiac condition may get turned down by insurers when he applies for a normal health insurance policy. Specialised cardiac plans can be a lifeline for them. “These plans allow people who may find it difficult to secure coverage through standard comprehensive plans to obtain insurance,” says Dubey.

The waiting period for covering pre-existing cardiac ailments could be short. “Coverage typically begins after a short waiting period of 90 days,” says Kapil Mehta, co-founder, SecureNow Insurance Broker.

Another positive, as Dodeja points out, is that people who buy a cardiac plan get covered for other ailments.

)

Limits on coverage

The coverage for pre-existing cardiac conditions could be capped. “This could mean out-of-pocket expenses for patients if they are hospitalised for a cardiac condition,” says Mehta.

These plans could come with some restrictions. “There can be sub-limits on room rents and modern treatments. Crucial benefits—like domiciliary treatment—might not be included,” says Dubey.

A standard hospitalisation plan may offer a wider array of daycare treatments and multiple refills of coverage in a year.

“A specialised cardiac plan may cover only a certain number of daycare treatments and allow for just one refill per year,” says Dubey. Some plans could also come with a co-payment requirement of, say, 20 per cent.

Specialised cardiac plans are generally costlier. According to Dubey, they could be 1.5-3 times costlier than a comprehensive policy. “The premium reflects the higher risk associated with covering a pre-existing heart condition,” he says.

Who should buy them?

Cardiac care plans are ideal for individuals with pre-existing heart conditions or a family history of heart issues. Those who can’t get coverage under a comprehensive plan should opt for these plans.

“If you have a mild cardiac problem and an insurer is willing to give you a comprehensive plan, go for it even if there is a loading,” says Mehta.

Points to heed

For individuals with heart ailments, buying a higher sum insured is critical.

“We recommend at least a Rs 20 lakh sum insured. As heart-related ailments can lead to multiple hospitalisations, a small sum insured of Rs 5 or Rs 7 lakh may not suffice,” says Siddharth Singhal, head–health insurance, Policybazaar.com.

Investors should watch out for co-payment requirement in these policies. “If the insurer offers the option and your pocket allows it, pay a higher premium and get the co-payment clause removed,” says Singhal.

Waiting periods for pre-existing conditions are also key. “Most plans have a three-year waiting period. However, some offer the option to reduce the waiting period to just 31 days. This is a highly beneficial feature for those with pre-existing conditions,” says Singhal.

A careful review of the coverage offered by the policy is essential. “Cardiac problems encompass a range of issues, so read the policy terms and conditions carefully to understand what is covered and what is excluded. Additionally, pay attention to the policy’s restrictions regarding room rent and total coverage,” says Mehta.

Check the policy’s network of hospitals so that availing the cashless benefit becomes easier.

Finally, customers should buy health insurance at a younger age so that they are able to secure a comprehensive policy. “Waiting until a health condition develops can limit choices,” says Dodeja.

The writer is a Mumbai-based independent journalist